Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin June 2025

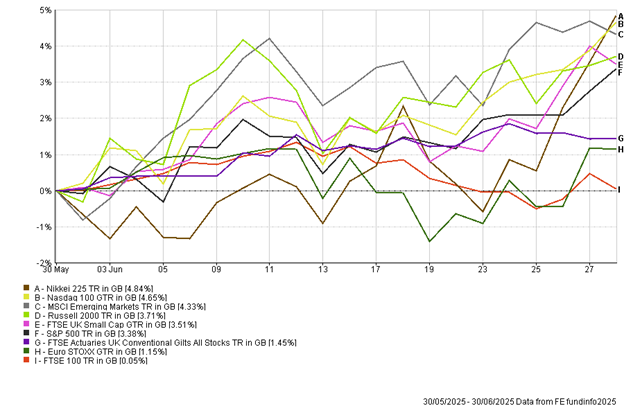

Markets had a positive June, as easing of geo-political tensions and optimism on future trade deals helped boost investor sentiment. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Volatility, Records and Renewed Optimism

In early June, Israeli airstrikes targeted Iranian nuclear infrastructure following suspected Iranian proxy activity in Syria. Iran responded with cyberattacks and limited missile retaliation. This raised fears of a broader Middle East conflict, especially around the Strait of Hormuz (a key global oil chokepoint). The oil price rose to $85 per barrel, as traders feared disruptions to supply routes. This resulted in a selloff in major global indices in early June, where defence and energy stocks outperformed on risk hedging.

However, after an agreed cease fire, the conflict between Israel and Iran—cooled off, which helped reduce volatility in oil prices and improve investor confidence. These developments allowed markets to focus more on fundamentals, such as corporate earnings and interest rates, rather than global risks.

The S&P 500, the benchmark for large U.S. companies reached new all-time highs, closing above 6,200 for the first time in history. The broader market was lifted by continued strength in major technology companies, solid corporate earnings, and improving global sentiment.

On the economic front, the data was mixed but mostly positive. Inflation continued to cool, which strengthened hopes that the Federal Reserve might start cutting interest rates later in the year. While the Fed didn’t make any changes in June, markets interpreted their messaging as more “dovish,” meaning they are leaning toward easing policy if inflation stays on track. Bond yields remained relatively steady, and the 10-year U.S. Treasury hovered between 4.2% and 4.4%, showing that investors were neither too worried about inflation nor expecting aggressive rate cuts just yet.

Emerging market and Asian stocks outperformed due to the US dollar falling to a three year low against major currencies and this combined with better trade dynamics with the US, attractive valuations and good corporate earnings helped lure investors to the region.

This was especially seen in Hong Kong listed technology companies and Indian mid-small cap companies due to robust domestic demand. In addition, commodity led exporters, which benefitted from rising energy, metals and agriculture prices in regions such as Brazil and South Africa also performed well. Overall, developed markets rose around 4.6%, and Emerging markets advanced 5.2%, for a sterling-based investor.

Looking Ahead…

There are reasons for both optimism and caution. The U.S. economy remains resilient, with steady job growth and solid consumer spending. Corporate earnings, particularly in technology, have been robust. However, some risks remain on the horizon. Political and geopolitical uncertainty are potentially not priced into markets, including U.S. fiscal concerns and uncertainty over tariff deals between countries still yet to be decided, which could introduce new volatility. And while inflation is easing, it’s not yet at the Fed’s target, meaning future interest rate decisions will remain data dependent.

As we highlighted in our Client Conference in January, the ever changing economic and geopolitical landscape leads us to maintain and focus on diversification across investment portfolios and year to date we have seen a much greater variety of returns compared with the previous US led focus in recent years. The broadening out of returns across regions, styles and market size year to date has been noticeable and highlighted within the table below.

|

Index |

Performance 31/12/2024-30/06/2025 |

| Euro Stoxx | 18.21% |

| FTSE 100 | 9.50% |

| FTSE UK Small Cap | 9.10% |

| MSCI Emerging Markets | 5.35% |

| FTSE Actuaries UK Conventional All Stocks (Gilts) | 2.50% |

| Nikkei 225 (Japan) | 0.83% |

| Nasdaq 100 (US Tech) | -0.98% |

| S&P 500 | -3.13% |

| Russell 2000 (US small cap) | -10.42% |

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Portfolio Changes

As we are at the half year point, we would be keen to highlight our year-to-date position and we have been focusing on finding investment opportunities outside the US, particularly with focus on tilting the portfolio to value global stocks ex US as foreign investors diversify their wealth out of the US, due to currency and political risk with rising trade uncertainty.

This has been reflected in our recent portfolio changes where we have sold iShares MSCI World Quality Factor ETF and bought Xtrackers Euro Stoxx Quality Dividend ETF. On a similar theme, we have also sold Schroder US Mid Cap Unit Trust and bought Artemis Global Income Unit Trust, to reduce our exposure to the US with reinvestment into mainly European equities based on expectations of returns broadening out away from the US.

In addition, we sold M&G Global Macro Bond due to fund manager departure and ongoing fund outflows with reinvestment into a global bond index by purchasing the iShares Aggregate Global Bond ETF for Cautious and Balanced Funds/Models only.

BOOLERS INVESTMENT COMMITTEE