Amandeep Mandair

Reveal Menu

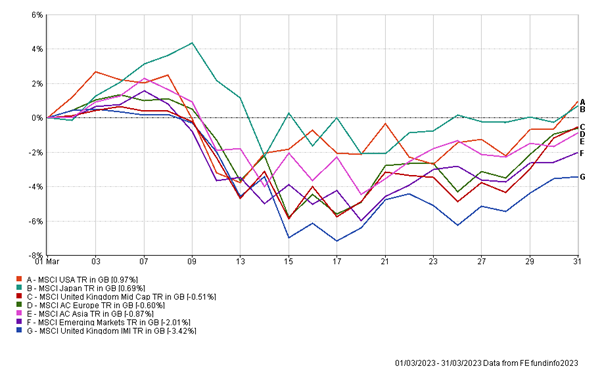

Market Commentary: Monthly Bulletin March 2023

It was a difficult month for markets after events in the global banking sector caused investor panic, but they recovered well in the final few weeks to end the first quarter of 2023 in positive territory. The performance of the main indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

As discussed in March’s emergency update, the collapse of Silicon Valley Bank (SVB), as well as the challenges surrounding Credit Suisse were unrelated events, but combined to cause a significant dent to investor confidence. The resulting sell-off, particularly impacting Global Financial sectors, was brutal and required both government and regulator intervention to stem the tide. In America, the Biden administration introduced stricter rules for mid-sized banks that included more rigorous liquidity requirements and more frequent stress testing which by month end appeared to have eased some of the investor concerns.

On the economic front, recent US inflation data was more positive for investors as the Fed’s preferred measure for inflation (PCE Index which excludes food and energy) came in at 4.6%, slightly below market expectations of 4.7%. The Fed followed through with another 25-basis points rate rise and although further hikes are expected, the terminal rate (peak point in a cycle), is now expected to be lower than previously anticipated. This despite a resilient labour market that showed the latest non-farm pay rolls grew stronger than expected by 311,000, pushing back on the notion of a recession later in the year.

The Bank of England followed America’s lead announcing a 25-basis point interest rate increase, the 11th consecutive hike putting interest rates at 4.25% and to their highest level since 2008. The latest inflation figures came in slightly higher than the previous month and with Bank of England Governor (Andrew Bailey) reiterating the view that the focus remains on curbing inflation, further tightening is expected. Like in the States, the UK economy has fared better than expected in the first quarter of 2023, with composite PMI’s in expansionary territory, supported by a boost in consumer spending and improved consumer confidence.

Elsewhere, the ECB announced an increase of 50 basis points at their monthly meeting, buoyed by a slowing of consumer price growth to 6.9% in the euro area, indicating that the tighter monetary policy was starting to take effect on the wider economy. European banks were particularly affected in March despite the takeover of Credit Suisse by UBS seeming to be swiftly and efficient transacted by Swiss regulators.

The China re-opening story continues to play a role in market movements, accommodative monetary policy by the People’s Bank of China and a rebound in economy activity so far in 2023 has seen investors look more favourably on the world’s second large economy. This has ripple effects into broader Asian and Emerging markets with the IMF recently estimating that China’s rebound may contribute to one around third of global growth this year.

Portfolio Changes

This month we diversified the make-up of our Fixed Interest exposure by equalising the allocations across our Strategic bond holdings. This increased exposure to our recent addition (the Premier Miton Monthly Income Bond fund) with the aim of reducing fund specific risk within Fixed Interest and better blending our holdings at the aggregate level to capitalise on the opportunities in the sector moving forward.

As always, should you wish to discuss your portfolio or markets more generally with your investment manager, then please do not hesitate to contact us.

THE BOOLERS INVESTMENT COMMITTEE