Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin March 2024

Markets ended the first quarter of 2024 positively, as stronger global growth and the potential for rate cuts fuelled a rally in cyclical sectors of the market. The performances of the main equity indices over the month are shown below.

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

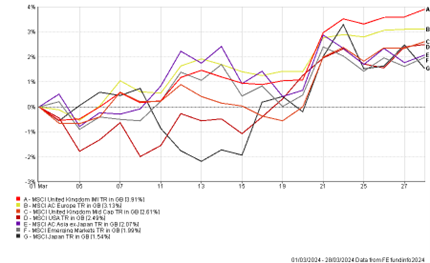

UK

UK equities performed well in March led by sectors such as energy, materials and financials, which outperformed in the hope that the Bank of England (BOE) would cut interest rates, helping to support stronger economic growth. The UK economy continues to make progress on inflation, with the rate of consumer prices increasing at a much slower rate in February at 3.4%, down from 4.0% in January and core inflation, which excludes energy, food and tobacco also slowing to 4.5% from 5.1% in January.

At their latest meeting, the BOE officials voted 8-1 to keep interest rates at 5.25% with no BOE officials voting for rate hikes. The BOE have communicated that they expect inflation to drop below its 2% target at some point in the second quarter due to the Chancellor’s decision at the March budget to freeze fuel duty which is projected to lead to lower energy costs. Although annual wage growth in the UK continues to remain high at 6%, it is expected to decline as consumer prices fall and businesses are not forced to pass higher costs on to consumers.

Source: Bank of England

US

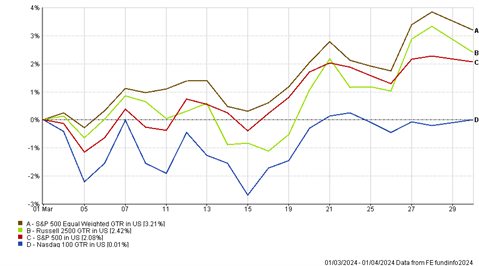

US equities continued to perform well in March with evidence of continued broadening out in the market, as sectors such as miners, energy, industrials all outperformed technology sectors over the month. This is a bullish sign for markets as it shows investors are looking for opportunities outside of technology and in undervalued cyclical areas of the market that tend to perform well in rate-cutting cycles. This is shown in the chart below, where the Equal Weighted S&P 500 Index & Russell 2500 Index (US small caps) outperformed the conventional S&P 500 index and the technology heavy Nasdaq 100 index in March.

In terms of the macroeconomic picture in the US, the probability of a first rate cut in June is now a 50/50 bet, as the latest US consumer prices remained sticky at 3.2% in February and producer input costs rose in February by 0.6% from the previous month in January. At their latest meeting, the US Federal Reserve (Fed) left rates unchanged at 5.25-5.50%.

In his press conference, US Fed Chair Jerome Powell signaled to investors that he acknowledged we are in a new era where inflation is going to stay higher than 2% in the long run due to the supply side shocks of a shortage of labour and a shift to deglobalisation post pandemic. Therefore, the strict inflation target of 2% may be more flexible going forwards, which would result in a higher chance of earlier rate cuts further down the line. He also reiterated that he does not want to leave interest rates too restrictive for too long which would result in a slowdown in economic growth.

(All figures are based on bid-to-bid pricing with income reinvested, in dollar terms)

Europe

In Europe, markets had a positive month as a result of improving consumer confidence, due to the mild winter and a rise in real wages due to falling inflation and a tight labour market. European consumers also have pent up savings, as a consequence of the perception that the energy crisis would be worse than expected.

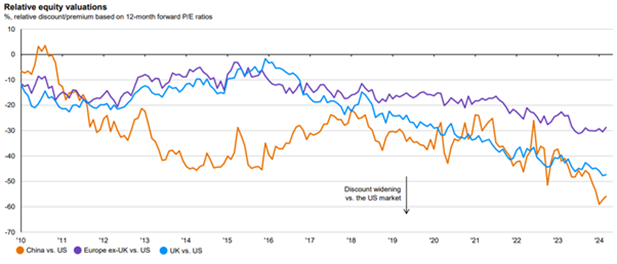

Investors expect a rebound in manufacturing which has now bottomed out and now in recovery mode as we approach a rate cutting cycle in the developed world, with consumers switching their spending back to goods from services, benefiting the likes of Germany and France. Valuations in Europe when compared to the US present good value with the one year forward P/E ratio for the MSCI US index being 21 times earnings and MSCI Europe index trading at 15 times earnings, thereby indicating a relative discount as shown in the chart below.

We are currently slightly underweight Europe, however, we are monitoring our position closely given the potential tailwinds, with a view to close this underweight at some point in the future as investors continue to broaden their investment horizons.

Source: JPMorgan Asset Management

Asia/Emerging Markets

Asia/Emerging Market equities underperformed Developed Markets (DM) in March, as investors continued to question the ability of the Chinese government to deliver the appropriate amount of fiscal policy to help boost consumer spending. The MSCI China Index has rallied 12.3% since the record low in January due to the short-term measures put in place by Chinese regulators to boost share prices of domestically listed companies, however, this rally may not be sustainable in the backdrop of slower economic growth than in the past.

Asia & Emerging Market equities are expected to catch up to the rest of the world this year as DM countries begin their easing cycle resulting in a weaker dollar lowering the value of dollar denominated liabilities and higher foreign direct investment.

In addition, EM & Asian countries have got a better grip on inflation because they did not follow with massive amounts of stimulus during the pandemic and consumers did not pursue the same behavioral shift as DM consumers of excessive spending on services, causing sticky service inflation in DM countries.

From a fundamental viewpoint, valuations in Asia/Emerging Markets remain compelling with Earnings Per Share (EPS) growth expected to beat DM equities over the medium to long-term starting from a much lower valuation base and this combined with a rate cutting cycle should result in positive gains for Asia/Emerging Market equities this year.

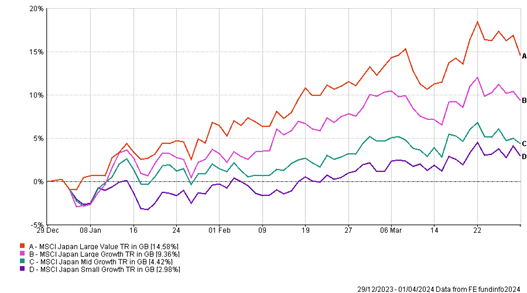

Japan

The Bank of Japan (BoJ) made a significant step to normalise their monetary policy by ending 8 years of negative interest rates by raising short term rates for the first time in 17 years to a new target rate between 0-0.1% range. The move by the BoJ was made after the announcement that the biggest companies in Japan agreed to raise wages for 2024 by 5% after negotiations with trade unions.

BoJ officials have communicated that although higher wages are positive for the economy, the plan is to go slow with the interest rate increases and phasing out its ultra loose monetary policy as they want to be sure that the rise in wages is sustainable in the long-term.

The impact of the move by the BoJ on financial markets has been a weaker yen compared to other major currencies due to the relative difference between interest rates between Japan and other western countries. The weaker yen has continued to support major large cap businesses that generate a significant proportion of their revenues outside of Japan. In terms of style, large cap value stocks have outperformed small and mid-cap growth-oriented stocks, as bond yields in the US and Japan have risen. In addition, foreign investors of Japanese stocks have been biased to large cap multinationals as they have essentially been buying ‘what they know’, leaving small and mid-cap companies out of favor.

Going forwards, we believe that as other central banks cut interest rates that the Yen should start to normalise and there will be a reversal of the trade, with investors rotating out of large cap stocks and into small and mid-cap stocks that are undervalued and under researched by the market.

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Portfolio Changes

This month we have sold our position in the JO Hambro UK Dynamic OEIC across our models because of the imminent departure of the lead fund manager, which has resulted in a significant increase in fund outflows, and we have reinvested the monies within the Artemis UK Select Unit Trust to maintain a core position in UK mid cap value stocks.

Furthermore, we have sold the iShares Edge MSCI Global Value Factor ETF across risk models and bought the iShares Edge MSCI Global Quality Factor ETF. This change was made to tilt our investment style in Global equities from Value to Quality/Growth to get more exposure to companies that have competitive advantages and are highly profitable regardless of the economic climate.

The final change this month has been to sell the Schroder Asian Alpha Plus Unit Trust and First Sentier Stewart Asia Pacific Leaders Sustainability OEIC within our Cautious risk models and buy Jupiter Asian Income Unit Trust. The reasoning behind these changes is to provide better risk management within Asian equities for lower risk clients by reducing exposure to China & India and to diversify further across other Asia Pacific regions.

THE BOOLERS INVESTMENT COMMITTEE