Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin March 2025

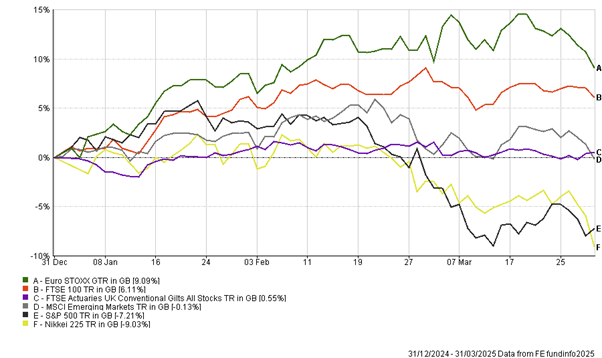

Despite the optimistic outlook at the beginning of 2025, the first quarter has seen a ramp up in volatility, particularly so for the US, and market performance diverged considerably from previous years, as per the chart below.

While some of the factors impacting markets were expected, others were more unforeseen, adding a layer of complexity to the broader market dynamics. Here’s a breakdown of the key causes:

1. Geopolitical Tensions

Ongoing geopolitical risks, especially the war in Ukraine, U.S.-China relations, and instability in the Middle East, significantly impacted investor sentiment in Q1 2025. Heightened fears of escalation in Ukraine, along with concerns about Chinese economic policies and tensions in Taiwan, introduced volatility in global markets.

2. Higher-Than-Expected Inflationary Pressures

While central banks like the Federal Reserve and European Central Bank had shifted towards a more dovish stance after a period of aggressive tightening, inflationary pressures remained elevated in certain regions. Energy prices, food costs, and wages continued to rise, leading to fears that inflation could be more persistent than expected.

3. Disappointing Economic Data

Despite expectations for economic recovery, some key economic indicators in Q1 2025 came in weaker than anticipated. The U.S. showed signs of slowing growth in certain sectors, particularly manufacturing and housing, as high borrowing costs continued to take a toll. In Europe, inflation remained high in some economies, while economic growth in southern Europe was slower than expected. This divergence in economic performance dampened optimism for a synchronized global recovery and contributed to a risk-off environment.

4. Valuation Concerns

As equity markets rebounded from the pandemic lows, concerns over stretched valuations began to surface in Q1 2025. The tech sector, in particular, had been trading at relatively high multiples, and some investors began to question whether these companies could maintain their rapid growth. A revaluation of growth stocks, especially in the face of higher inflation and uncertain economic conditions, led to a pullback in some of the most highly valued names.

5. Rising Bond Yields

As inflation remained persistent in certain regions and economic growth showed signs of slowing, bond yields began to rise again. Higher yields made bonds more attractive relative to equities, particularly dividend-paying stocks. This shift in investor preference towards fixed-income assets led to a decline in equity prices, especially in growth and tech sectors, which are more sensitive to interest rate changes.

6. Trade Tariffs

Saving the ‘best’ until last, President Trump and his constant trade tariff rhetoric unsettled markets and fuelled concerns over the impact to economic growth. The uncertainty around the tariffs and at what level they will be implemented, if they will be reduced or have exceptions has added uncertainty for growth forecasts and created generally weaker sentiment.

Summary

In our client conference at the end of January, we highlighted various potential outcomes for markets covering the risk-on, risk-off and ‘more of the same’ scenarios. Over the last month or so, we have certainly been in a risk-off environment for the US market, as trade tariff threats and concerns over growth led to investors reevaluating their positions. This was all not focused on the highly valued tech sector and the growth fears also impacted the smaller end of the market.

Europe on the other hand fared much better given the boost from a commitment to increase defence spending across the region and whilst Europe has benefited in the short-term, how long this newly found optimism lasts is still uncertain as there are still many political and economic challenges to overcome.

Looking back on the quarter, to some extent a cooling of US exceptionalism and euphoria over large cap tech stocks is not the worst outcome, given the broadening out of returns to other regions. We may well have seen an overreaction in the short term within the US but we remain mindful of the continuing volatility, particularly around US tariffs and retaliatory action from other countries. We have said many times that the one thing that markets do not like is uncertainty and we are hopeful that once some certainty over the tariff position is provided, and ultimately how this is likely to impact on economic growth, then markets can stabilise and move forward.