Amandeep Mandair

Reveal Menu

Market Commentary: Monthly Bulletin May 2022

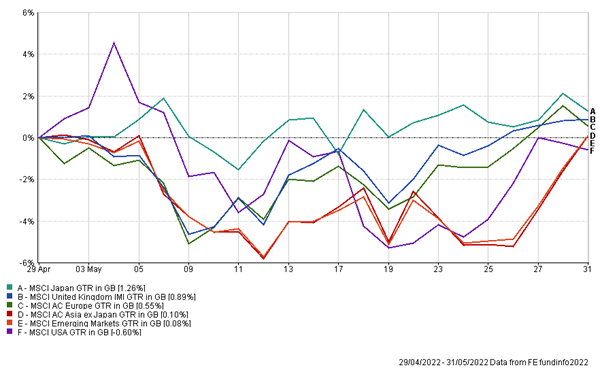

Market volatility remained elevated during May, as hawkish pivots by Global Central Banks continued to pressure investor sentiment and signs of softening in economic data weighed in on market movements. The performance of the main indices are highlighted below:

The Fed reiterated a hawkish view at the start of the month, raising interest rates from 0.5% to a target rate range between 0.75%-1%, in its largest hike since 2000 in a bid to dampen soaring inflation, with the view to continue raising rates until inflationary pressures begin to ease off. However, the most recent Fed minutes released end of last week, surprised to the upside with some members of the Federal Open Market Committee indicating a more restrictive approach to tightening policy as first anticipated as economic uncertainty remains.

The S&P global flash US PMI (Purchasing Managers Index, which indicates the robustness of sector) was revised down from its April’s reading to 57.5, as input and output costs increased as well as net sales growth slowed, as business activity moderated. With economic data indicating a more subdued outlook, it is in the Fed’s best interest to monitor its aggressive policy to achieve a soft landing for the economy over the coming months amid a tighter labour market and slowing growth.

The Bank of England continues its path of interest rate hikes, increasing rates to 1% in its latest meeting, the highest level since 2009. Bank of England’s chief Economist Huw Pill remained closely aligned to its original objectives to curb inflation, reiterating the view further interest rate hikes and policy tightening is sufficient in easing elevated price pressures, however the importance of the level of tightening is crucial to avoid a deep recession.

In addition, the Chancellor, Rishi Sunak recently announced a fresh round of government backed fiscal stimulus in the shape of £15 billion, in an aid to support poorer households through the painful spike of energy prices as the cost-of-living crisis worsens.

Although this may be a ‘kicking the can down the road’ scenario, it may ease the pressure off the Central Bank in the short term, thus inflation control can remain its key focus.

The European Central Bank, who are substantially behind the curve compared to their western counterparties unveiled a more stringent monetary policy over the month, confirming an early end to its bond-buying program in the third quarter of the year, with a rate hike as early as July, with the intentions to shift out of negative rate territory by Q3. Economic data reflected a more muted economic outlook as PMI data for both manufacturing and services notched down in May, as economic uncertainty and geopolitical tensions persist.

China’s economic woes also weighed in on investor sentiment over the month, as a slowing GDP growth as well as the zero covid policy led to market declines. GDP growth is projected to slow to 4.8% over the course of the year, the slowest pace since 1979. Conflicting views between the President Xi Jinping and the Principal Advisor Li Keqiang, on the balance between economic growth and pandemic controls has led a divergence in policymaking, however with cities such as Shanghai easing lockdown restrictions, this should see some shifts in supply chain disruptions globally alleviate over the following months.

During this volatile period in markets, we continue to manage our portfolios with the belief that equity-based investing remains appropriate over the medium to long-term and investors who are patient and adopt such an approach, will ultimately be rewarded. We of course monitoring markets closely and will take any appropriate action we deem necessary to adapt to the continuously changing macro-economic and geo-political environment.

Reporting

The quarterly investment reports were issued last month and these will be followed by the quarterly Custody Statements. These detail each of investment holdings that are held in nominee on your behalf by Pershing and are a regulatory requirement. Both of these documents are uploaded electronically to the investor portal and this can remove the need to issue paper copies. Please contact us if you would like to register for the portal and we can send through the required registration link.

Finally, the annual consolidated tax reports will also be issued shortly and we will have electronic copies if required.

If you have any queries regarding your portfolio, please do not hesitate to contact your investment manager.

THE BOOLERS INVESTMENT COMMITTEE