Amandeep Mandair

Reveal Menu

Market Commentary: Monthly Bulletin May 2023

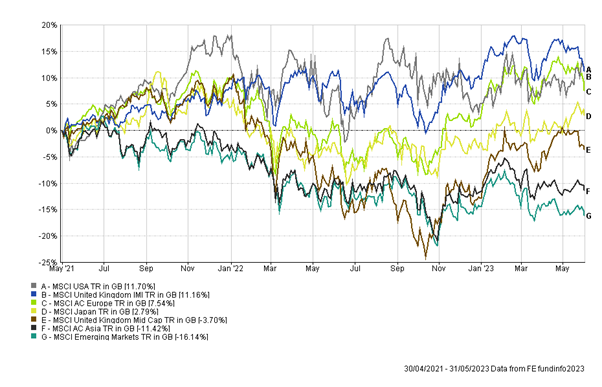

Market indices remained mixed over the month, with developed countries showcasing positive returns as better than expected economic data across US, UK and Europe provided markets with optimism amid an uncertain economic backdrop. The performance of the main equity indices is summarised below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

US

The debt ceiling debacle in the US took centre stage as investors watched closely for signs of progression and at the last hour the Republicans and Democrats agreed on a bill which means that the federal government will not be in a position to default on debt payments ahead of the June 5th deadline.

Inflation also remained high on the agenda as April’s figure saw a temporary incline by 0.4%, nonetheless year over year gains at 5% remain low in comparison to previous readings, with markets expecting a falling inflation trajectory to continue. Hawkish comments from the Fed led to investors pricing in a higher probability of a further hike in June as job openings rebounded to 10.1 hitting their highest level since January, as resilience to some areas of the US economy may lead to a tighter monetary policy for longer.

Following the G7 Summit in May, a de-escalation in China and US tensions led to a narrow rally in US markets, with Biden reiterating a more positive rhetoric on relations between the two nations.

Europe

The European Central Bank delivered a further 25 basis point hike in its latest monetary hiking cycle to curb inflationary pressures although headline inflation fell to 6.1% from the previous month’s 7.0%, with a further two rate hikes expected over the coming months. In addition, flash composite PMI data in Manufacturing and Services for the Euro area edged lower to 44.8 and 55.1 respectively, indicating a slowing in economic momentum, albeit Services PMI remains in expansionary territory.

UK

The Bank of England also continued their tightening cycle with a further 25 basis points increase to 4.5%, with the latest commentary from the committee stating signs of persistent inflation, which will lead to further hikes if required. Latest inflation figures saw a decline in headline CPI fall from 10.1% to 8.7%, however this was still above market expectations, therefore reiterating the view monetary tightening may need to last longer than anticipated in order to bring the cost of living lower.

Japan

In the Far east, investor sentiment increased as the Bank of Japan’s key inflation measure showed an increase to 4.1% year on year, the biggest rise since 1981 and indicating the economy may finally making its way out of stagnant deflation. The Nikkei 225 benchmark experienced a 33 year high during May, supported by upbeat economic data (services sector reported robust growth trending in expansionary territory at 55.9). A potential economic revival in Japan, paired with strong foreign investor interest and strong domestic earnings may lead interesting opportunities in this arena.

Emerging Markets

In China, a second month of falling PMI data down from 49.2 to 48.8 in contraction, indicated a drag caused by declining new orders and exports. Industrial profits also experienced a decline of 20.6% in the first four months of the year, amid slowing external demand, as impacts of stickier inflation and tighter monetary conditions, weigh in on the wider global economy. Flagging property sector growth as property investments fell 6.2% year on year, following China’s reopening at the back end of last year, indicates additional measures may need to be taken as current government stimulus is starting to wear off.

Portfolios

Portfolios moved broadly in line with market indices over the month, however outperformed their respective benchmarks. Portfolios remain fully diversified and invested amid a backdrop of economic uncertainty and ongoing headwinds, with the longer term view a blended approach in portfolios remains appropriate.

As always, should you wish to discuss your portfolio or markets more generally with your investment manager, then please do not hesitate to contact us.

The Boolers Investment Committee