Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin May 2026

Key Points

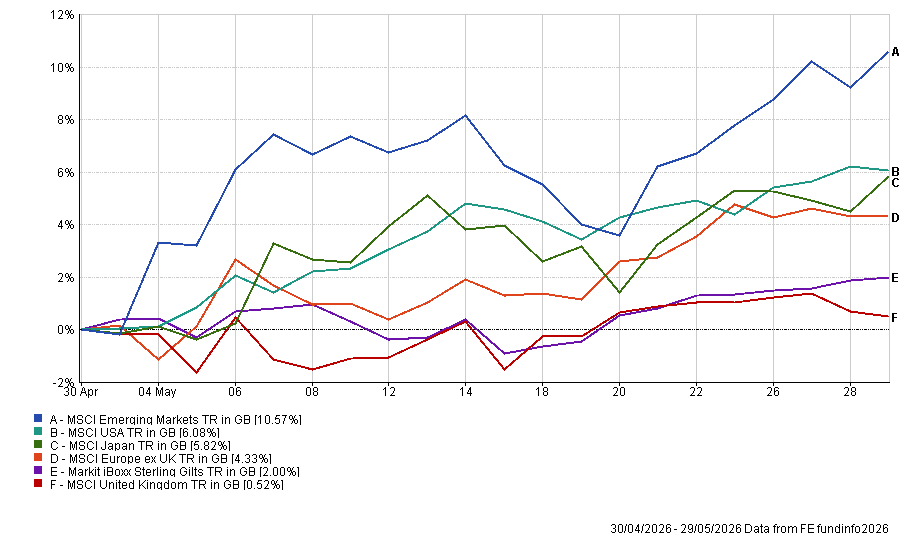

May built on the recovery seen in April, with markets proving more resilient than many had expected despite ongoing geopolitical tensions, elevated energy prices and uncertainty over interest rates. Several major equity indices remained close to record highs as investors focused on company results, the outlook for inflation and signs that central banks may not need to tighten policy further in the near term. The performance of the main indices over the month is provided below for reference.

(All figures are based on bid-to-bid prices with income reinvested in Pounds Sterling. Source: FE fundinfo 2026)

Strong Earnings Continue to Support Equity Markets

One of the most striking features of May was the ability of equity markets to stay firm in the face of an unsettled backdrop. Company results continued to come through better than expected, particularly in the United States, where large technology businesses again demonstrated strong profit growth and resilient demand. Investors remained especially focused on the role of artificial intelligence, with spending on data centres, software and digital infrastructure still acting as a major driver of earnings momentum.

This helped keep global markets well supported through the month, even though valuations in some areas remain elevated. Importantly, the rally was not driven purely by optimism. It was backed by real earnings growth, improving margins and evidence that many businesses are continuing to adapt well to higher costs and a more challenging economic environment. For clients, this is a useful reminder that markets can often look through near-term noise when company fundamentals remain healthy.

UK Inflation Cools, Giving the Bank of England More Breathing Space

Another important theme in May was a shift in expectations around UK interest rates. Inflation data released during May showed that April’s headline CPI rate eased to 2.8% from 3.3% in March. At the same time, retail sales weakened and there were further signs that parts of the UK economy are losing momentum. Together, this reduced market concerns that the Bank of England would need to raise rates again immediately.

For investors, that matters because interest rate expectations influence both bond markets and company valuations. A less aggressive path from the Bank of England was taken positively by UK shares and helped to ease pressure on bond yields. It does not mean inflation has been defeated, as it is still expected to tick up in the short term, nor that rate cuts are guaranteed, but it does suggest that policymakers may now have more room to pause and assess the economic impact of higher energy costs. That is a more constructive backdrop than markets had feared earlier in the spring.

Energy Prices and Geopolitics Still Matter

Although markets were calmer during much of May, the backdrop was still heavily influenced by developments in the Middle East and the effect on global energy supplies. Oil prices remained elevated by historical standards, with Brent Crude ending the month at $92 per barrel, and while there were occasional signs of easing tensions, investors remained alert to the risk of renewed disruption. Higher energy prices continue to feed into inflation expectations, business costs and consumer confidence, which is why markets remain so sensitive to events in the region.

What May demonstrated, however, is that investors are becoming more selective and more measured in how they respond to geopolitical headlines. Rather than triggering a broad market sell-off each time tensions flared, the impact was more contained, particularly when earnings and economic data remained supportive. That does not remove the risks, but it does reinforce the value of staying diversified and focused on long-term fundamentals rather than reacting to every short-term shock.

As we move into June, the key questions for markets remain broadly the same: whether inflation continues to moderate, whether central banks can avoid tightening policy further, and whether geopolitical tensions begin to ease in a more lasting way. For now, May has shown that markets can still make progress even in an environment where risks remain very real. Against this backdrop, we remain selective, diversified and focused on long-term opportunities rather than reacting to short-term market noise.

Portfolio Positioning

Towards the end of the month, we reduced cash levels across our three OEIC funds slightly, from 5% to 4.5%, reflecting continued earnings strength, ongoing capital investment and improving sentiment towards technology shares, particularly those exposed to AI-related themes. In the Balanced and Adventurous funds, we used this modest increase in market exposure to add to the Polar Global Technology Fund, with the aim of capturing longer-term growth opportunities. In the Cautious Fund, we added to the Schroder Strategic Bond Fund instead, helping to maintain the portfolio’s defensive characteristics, diversification and overall risk management for lower-risk clients.

BOOLERS INVESTMENT COMMITTEE