Amandeep Mandair

Reveal Menu

Market Commentary: Monthly Bulletin November 2022

Markets

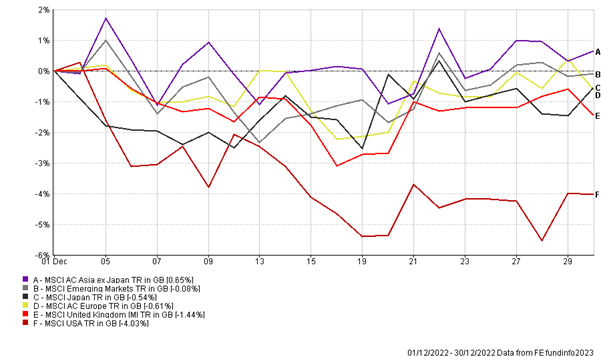

As we come towards the end of the year, financial markets continued to recover, following signs of peaking inflation despite headwinds from an ongoing tighter monetary policy regime. The performances of the main indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Macro indicators in the US pointed towards a more resilient economy than expected, with retail sales figures released in October showing growth of 1.3% compared to the previous month. This paired with a strong labour market, the economy is holding up better than expected. In addition, there were also signs of peaking inflation in the US as supply chain disruptions continued to ease, leading to inflation falling to levels of 7.7%, however some areas of the economy seem to be stickier than others such as food and services indicating inflationary pressures remain in the near term.

Central banks continue to dictate market movements as both the Federal Reserve and the Bank of England raised policy rates in November. The Fed hiked interest rates by a further 75 basis points to 4%, however recent commentary by Jay Powell signalled a smaller interest rate hike may be on the cards as early as the FOMC meeting which will take place in mid-December, as the effects of tightening will take time to filter through into the wider economy. That being said, the Fed also highlighted the implications of relaxing interest rate hikes too soon and therefore elevated interest rates may last longer.

The Bank of England also followed suit, hiking rates to 3%, with hikes to continue into December with an expected 50 basis points hike, followed by quarter point hikes in Q1 2023. On the contrary, housing market showcased signs of cooling as a survey conducted by mortgage lender Nationwide exhibited house prices falling in November by 1.4%, the biggest decline since the coronavirus lockdown. Historically the BoE have paused interest rate hiking when house prices have displayed year on year contraction, as a result, if the UK economy continues to deteriorate paired with a slowing housing market the MPC may decide to pause monetary policy tightening sooner.

ECB’s Christine Lagarde also hinted at further rate hikes as inflation in the Eurozone shows little indication of peaking and could even accelerate further in the coming months amid the energy crisis. In October, energy costs in particular regions rose by circa 24% and with price increases having a lagged effect in being passed through to the end consumer, the pinch of rising costs will be continued to be felt into next year. On the other hand, positive PMI data showed an uptick in consumer confidence, which supported a rally in equities towards the end of November.

Emerging market equities experienced a sharp rally, as China announced measures to relax its zero covid policy regime. This included shorter quarantine periods as well as vaccination initiatives to help immunise elderly at a quicker pace. China’s senior official in relation to the Coronavirus response, Sun Chunlan, reiterated the view efforts to combat the virus is entering a new phase, with Beijing indicating it is moving closer to reopening its economy. Nonetheless, the Chinese economy remains under pressure as retail sales came in weaker than expected down -0.5% year-on-year indicating growth continues to slow in the region.

Overall, as we come towards the end of 2022, bond and equity markets have somewhat recovered from steep losses earlier on in the year, caused largely due to geopolitical and global economic uncertainty. Although, macro indicators still point to a mild recession in 2023, supply chain disruptions easing, as well as signs of moderating inflation in areas of the global economy, provides optimism for markets over the longer term.

Our portfolios continue to be invested in equity and non-equity assets, diversified across different geographical regions, sectors and companies. We still believe equities will continue to outperform other asset classes over the medium to long-term, as company fundamentals remain intact.

As per our previous updates, we believe that long-term investors should stay fully invested and our blend of Value, Growth and Quality-oriented equity funds means that portfolios are well positioned to benefit from any style rotation and recovery in markets.

Over the month our risk models have moved broadly in line with markets, outperforming their respective benchmarks and peers, which has been a common trend thus far this year.

As always, should you wish to discuss your portfolio or markets more generally with your investment manager, then please do not hesitate to contact us.

THE BOOLERS INVESTMENT COMMITTEE