Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin November 2024

November was a positive month for most developed markets, as investors received more certainty on policy following the election of Donald Trump as US President and positive news on global corporate earnings for the third quarter. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

The Return of the MAGA

The US election was won convincingly by Donald Trump, with a clean sweep for The Republican Party in the White House, the Senate and the House of Representatives. US equity markets have risen to all-time highs, as investors see Trump as a positive for Corporate America with the agenda of tax cuts, trade tariffs, increased government spending and reduced regulation, all of which are expected to increase US corporate earnings.

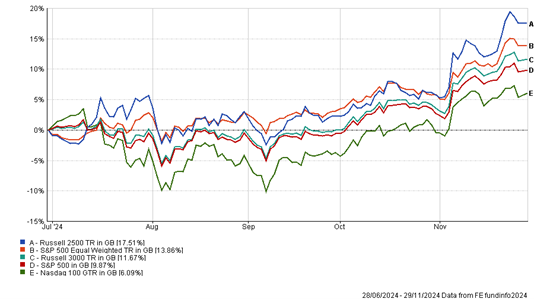

So where do investors want to be positioned? Historically, looking back to 2016 when Trump was last elected, sectors such as financials, industrials, defence and energy outperformed. This very much focuses on domestic stocks and more so the mid-smaller end of the market cap spectrum. This certainly plays into the general broadening out argument and, as shown in the chart below, we have already seen this in the second half of 2024 so far with small-mid cap companies having outperformed the tech heavy and expensive S&P 500 and Nasdaq 100 indices.

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Resilient Earnings Support Lofty Valuations

This year has been positive for global equity markets and particularly so for the US and mega cap technology companies, which has resulted in higher valuations. Looking at the forward P/E (price to earnings) ratio, the S&P 500 is currently valued at 22 times and is notably higher than the 5- and 10-years averages, 19.6 and 18.1 respectively.

Investors have been happy to continue to pay these higher valuations on the expectation that companies will continue to grow their earnings and either reinvest for future growth or pay out dividends to shareholders.

Certainly, for now, earnings have been much more resilient in the US and for example third quarter earnings season has been positive overall with 75% of S&P 500 companies having reported a positive earnings surprise and 61% of companies reporting a positive revenue surprise. At the sector level, eight of the eleven sectors are predicted to report year-over-year earnings growth in Q4 2024.

Portfolio Changes

Following the US election and supported by comments above, we have increased our US exposure adding to our existing position in the Invesco S&P Equal Weight ETF. To fund this move we have reduced fixed interest exposure for Balanced and Adventurous investors by trimming M&G Global Macro Bond and Vanguard UK Government Bond funds respectively. For Cautious clients, we have trimmed our Emerging Market exposure by reducing the Fidelity Emerging Markets fund.

THE BOOLERS INVESTMENT COMMITTEE