Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin November 2025

Welcome to the November edition of our Market Commentary

Each month, we bring you a clear and concise overview of key developments shaping financial markets – designed to keep you informed and confident in your financial journey.

In this issue, we will explore:

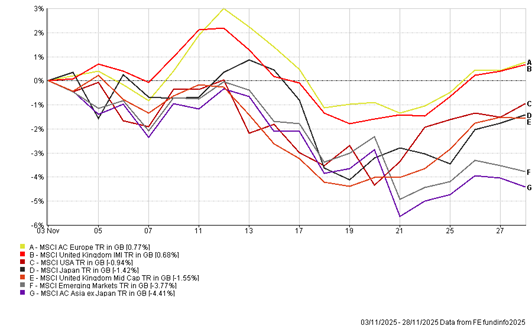

Markets: Monthly Performance

Global equities extended gains early in November, supported by strong Q3 earnings (82% of S&P companies beat estimates) and AI-driven growth in mega-cap tech. This proved to be short lived with volatility returning on the back of AI bubble fears and robust jobs data tempering expectations for imminent Fed cuts. European equities outperformed on fiscal expansion and defence spending themes, along with Japanese stocks bouncing back, as pro-growth policies and household stimulus plans boosted investor sentiment.

The performances of the main equity indices are highlighted below:

(All figures are based on bid-bid prices with income reinvested, unless otherwise stated)

UK Equities: Budget Reaction

Despite all the speculation and fanfare, Rachel Reeves finally delivered her Autumn Budget last week and encouragingly, it turned out not to be the big event that many (including us) had expected.

A budget focused on tax increases and welfare reform, she resisted the temptation to break manifesto pledges in more contentious areas, such as Income Tax, pleasing many, and was rewarded for doing so. Equity market reaction was muted, which we took as a positive sign.

Arguably, a better barometer for the Chancellor was the small improvements in Sterling and Government Debt markets that were as much relieved as they were pleased with some of her announcements. The increase in Fiscal Headroom (rising to £21.7 billion) is undoubtedly their big win, allowing for greater fiscal flexibility moving forward and ultimately reducing vulnerability.

Whilst most agree that this budget provides a degree of stability (for now), it may not be enough to increase the business confidence and economic growth so desperately needed. The OBR (Office for Budget Responsibility) estimated the budget policies “would have no significant impact on overall economic output (GDP) by 2030” and they have already revised down Economic Growth and Productivity expectations, whilst Inflation was revised up. More work needs to be done.

Crypto Assets: Sentiment Turns South

Crypto markets endured a sharp and disorderly sell-off in November, with Bitcoin, Ethereum and most altcoins tumbling heavily. Bitcoin experienced a particularly notable move, falling from its October peak of around $126,000 to just over $90,000 by the end of the month, effectively erasing all of its gains for 2025 as illustrated in the chart below.

This decline was driven by a shift in broader market sentiment as investors grew more cautious about higher-for-longer interest rates, alongside the unwinding of leveraged positions within the crypto ecosystem. As prices fell, many traders using borrowed money were forced to liquidate, accelerating the downturn and triggering widespread panic selling across the sector.

By late November, the worst of the forced selling had washed through, and prices began to stabilise, with Bitcoin showing a modest recovery in the final days of the month. However, sentiment across the space remains fragile, and smaller cryptocurrencies continue to lag as liquidity stays thin and investors rotate back towards safer assets. Overall, November served as a clear reminder of how quickly crypto can react to shifts in confidence and macro expectations.

Equities: Storms Gathering

Forward P/E ratios for major US indices are well above long-term averages, giving investors little room to manoeuvre if growth slows or earnings disappoint. The rally this year has increasingly become concentrated in a handful of large-cap tech names. Broader market participation is still weak, with mid/small cap companies underperforming. Historically, such narrow breadth signals vulnerability to sharp corrections.

Inflation is moderating, but unevenly, which is increasing the risk of policy missteps, and central banks are at a crossroads, while markets expect rate cuts, recent labour market and inflation data suggest policymakers may delay easing. A hawkish surprise from the US Federal Reserve and European Central Bank could trigger repricing across global equities.

In such times, we stay defensive by not chasing narrow technology led rallies but instead prioritising solid company fundamentals. Focusing on quality companies with strong balance sheets and by balancing equity exposure with short-and medium-term fixed income and alternatives, for an added layer of protection.

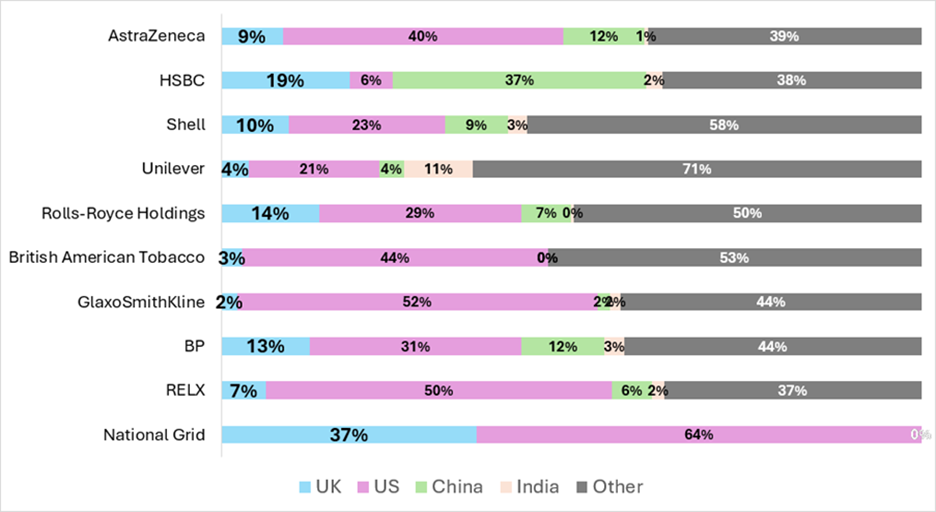

Chart of the Month:

We occasionally hear concerns from clients about our UK equity exposure, which they conflate with the UK economy. However, if we look at where the FTSE 100 companies make their money, less than 25% comes from the UK. The chart below shows the current top ten companies, with their UK revenues highlighted in light blue.

Source: FactSet/7IM

There are many reasons why individual UK companies behave very differently from the UK economy, but the above chart provides a stark illustration of how little dependence they have on it. A less misleading description of these UK companies would be global companies that happen to be listed in the UK.

Portfolios: Cash is King

During the month, we have seen further inflows into the Boolers OEIC as existing Advisory clients have started to move assets over into the more actively managed OEIC funds. As flows have come into the funds, we have taken the decision to retain reasonably high cash weightings (6-7%) across each fund, given the volatility we have experienced over the month and reflecting the general comments above.

We are keeping a close watch on short term developments and how/if we provide greater protection, whilst still balancing the longer term aims of generating competitive returns for clients.

BOOLERS INVESTMENT COMMITTEE