Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin October 2023

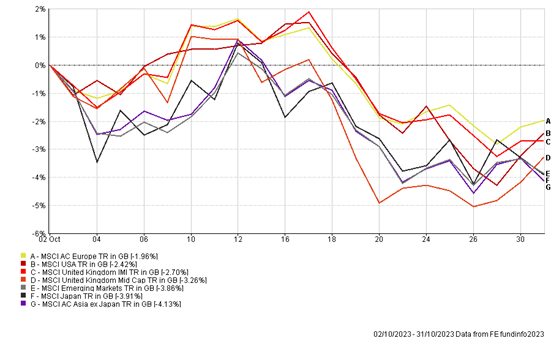

Markets were negative for October, as higher bond yields and geo-political uncertainty put pressure on equity valuations. In addition, positive economic data in the US signalled to markets that a recession could be delayed further, meaning interest rates remaining higher for longer. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Geopolitics

In October, we saw an escalation of the Israel and Palestine conflict, as result of a surprise attack from the terrorist group Hamas. So far, the spillover for markets has been a slightly higher oil price, as some Arab oil rich nations such as Iran, Syria, and Saudi Arabia were perceived to give their support to Hamas for the attacks.

For now, investors are putting a further escalation of the conflict (where we would see major countries taking more action to get involved), to the back of their minds and are focusing more on global interest rates and inflation. The outcome of any further escalation is that the oil price moves significantly higher and remaining elevated for longer, which may result in central banks being forced to raise rates above current levels.

However, we believe that any rise in the oil price will remain temporary because of the slowing of the global economy, particularly in key economies such as China (who contribute a third to global growth output) where growth has been sluggish by their standards due to a fall in consumption and a struggling property sector. Therefore, demand is unlikely to be strong enough to keep energy prices artificially high over the medium to long-term. As of writing the Benchmark Crude oil price currently trades at $85 dollars a barrel.

North America

The US economy continues to remain strong as the latest data showed annualised GDP growth for Q3 to be at 4.9%. Moreover, despite job openings falling and lower private sector payrolls, the labour market continues to remain tight with the unemployment rate at 3.8%. This puts pressure on wages to remain higher than the normal trend rate of growth, leaving inflation above the 2% target rate.

Therefore, markets have been pricing interest rates to remain higher than originally expected, with now a lower probability of early interest rate cuts next year, causing bond yields to trade higher. When bond yields rise, they put pressure on all risk assets, especially those assets that have higher valuations such as the magnificent seven technology stocks (Apple, Amazon, Google, Nvidia, Microsoft, Meta, Tesla), which have outperformed this year, as higher yields mean the present value of their future earnings fall.

Despite the resilience of the US economy so far this year, there is evidence that the economy is starting to slow in the most interest sensitive sectors such as housing, as mortgage rates are now at 8% and in auto-car loans, where more consumers are falling behind monthly payments, particularly those on low-middle incomes. The US Federal Reserve has been raising interest rates for the last 18 months and on average there is normally an 18-month time lag before we really to start to see the full effects of the first few interest rate increases on the economy.

As we move through into the next year, we should see a slowdown in economic growth as both consumers and businesses reign in their investment and spending. This should result in a rise in the unemployment rate, pushing down wage pressures, which in turn will result in the US Federal Reserve to be in position to cut interest rates, which will be a tailwind for risk assets.

UK

Similarly in the UK, we have yet to see the full effects of rising rates on the economy, with economic data showing business activity in the private sector slowing in the last few months. The dilemma for the Bank of England is whether to continuing increasing interest rates further, with the latest data showing headline consumer inflation remaining elevated at 6.7%. Wage pressures may have peaked, with most of public sector pay rises taken place through this year and the recent rise in energy prices from the Israel-Palestine conflict likely to be transitory. Therefore, it is expected that the Bank of England will leave interest rates on hold at 5.25% in their November meeting, with markets pricing only a 10% probability of a rate rise now.

Japan

In the land of the rising sun, the Bank of Japan (BoJ) left interest rates unchanged at -0.1% but took a significant step towards to normalising monetary policy by allowing the 10-year Japanese government bond yield to rise to 1%, revising its so-called yield curve control policy. The reason for the change in policy was because of the rapid rise in treasury yields, which put pressure on the Japanese Yen (which is down 12.8% against the US dollar this year) and due to the latest annual inflation rate remaining at 3.0% for September falling from 3.2% from the previous month.

The BoJ maintain that they need to see more signs that the wage growth is sustainable and long lasting to ensure the economy does not fall-back to stagnant deflation as seen in the last few decades. Therefore, for now the BoJ are prepared to leave interest rates lower for longer, as shown by their recent intervention at the beginning of October to increase purchases of 10-year Japanese government bonds, keeping the yield below 1%.

Summary

We acknowledge that markets and the global economy are currently going through a volatile time, and you may have concerns regarding your investments. Our portfolios continue to be managed with a view that over the long-term, equities will overcome these macroeconomic and geo-political challenges and a well-diversified portfolio is key to help mitigate risk in times of short-term market volatility and will ultimately be rewarded over the longer term.

We are continuing to monitor events closely and looking to take advantage of buying opportunities, having increased our cash weighting in recent months. As always, if you have any queries regarding your portfolios, please do not hesitate to contact your investment manager.

THE BOOLERS INVESTMENT COMMITTEE