Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin October 2024

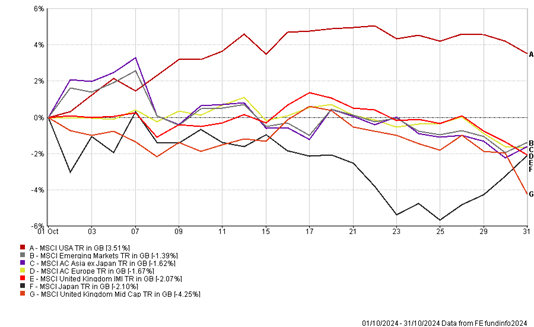

October was a mixed month for markets, with all eyes on the Autumn budget, the US election and key economic data from the US. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Budget 2024

Whilst UK equity markets were mixed, the FTSE AIM All Share Index bucked the trend rising 4% on the day after the announcement that 50% Business Relief was still available, after a holding period of 2 years, and avoiding a full assessment to Inheritance Tax. This highlights the vital role UK small cap/AIM companies play in UK economic growth. With interest rates expected to continue to fall this year and growth remaining robust, small cap stocks trade at attractive valuations with great upside for long-term investors.

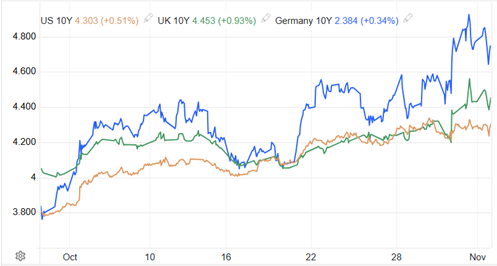

The most significant move in UK assets was in the gilt (government bond) market with yields rising in the aftermath of the budget, with the benchmark 10-year gilt yield increasing to a one year high of 4.5% before falling back slightly as investors locked into higher attractive yields. The bond market has been digesting fiscal rule changes announced by the Chancellor which will increase borrowing for investment by approximately £53 billion over the course of this parliament.

So, what does this mean for the outlook for gilts? We are hopeful that the gilt market will stabilise, as the Bank of England gradually reduces its Quantitative Tightening program and continued demand from institutional buyers such as banks and pension funds, should be supportive of the bank treasury and the UK bond market.

Follow the Bond Yields

In the run up to the Autumn Budget, bond yields have not only been rising in the UK market but also globally. In the US, the benchmark 10-year treasury yield has increased by over 15% since the start of the October due to concerns that the next US President (be it Trump or Harris) will borrow to increase government spending which will result in a higher issuance of US bonds in the treasury market.

With US debt to GDP at near record highs already, at some point investors need to be given reassurance that governments will get serious about being fiscally prudent. Therefore, when it comes to buying their government bonds investors will demand higher yields before jumping to secure their portfolios with US treasuries.

Source: Trading Economics

US Resilience

Latest figures show that the US economy grew at an annualized rate of 2.8% in the third quarter, a sign that the US consumer is still in a strong position even as core consumer price inflation has remained elevated at 3.3%.

In September, the US Federal Reserve (Fed) cut interest rates by 0.5%. This is likely to support further economic growth in the US, with an easing of monetary conditions helping consumers with car loans and credit card debt. There are no signs of the labour market slowing down, rather conditions appear to be improving, with initial jobless claims decreasing by 12,000 to 216,000 based on the latest weekly numbers. This so called ‘US Exceptionalism’ has resulted in continued improvement in company earnings, leading to strong performance in mega/large cap US stocks.

With growth remaining resilient, the Fed is likely to follow a slower path to cutting interest rates with potentially no further cuts this year.

Portfolio Changes

Earlier this month, we sold our UK Gilts position in the Vanguard UK Government Bond Index fund in anticipation that the Autumn budget would result in volatility within the Gilt market. Given the initial reaction to the Budget, we have been able to take advantage and reinvest back into the Vanguard fund at more favourable levels, locking in higher yields and taking advantage of any future capital appreciation as rate cuts occur.

The Boolers Investment Committee