Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin October 2025

Key Points

Markets

Global equity markets extended their rally in October as softer US inflation and a second consecutive Federal Reserve rate cut supported equities. However, a continued US government shutdown and geopolitics kept volatility alive. Global indices notched another positive month, aided by mega‑cap tech Q3 earnings beats and gold traded in record territory. The dollar ended higher after the Bank of Japan (BoJ) and the European Central Bank left rates unchanged. The performances of the main equity indices are highlighted below:

(All figures are based on bid-bid prices with income reinvested, unless otherwise stated)

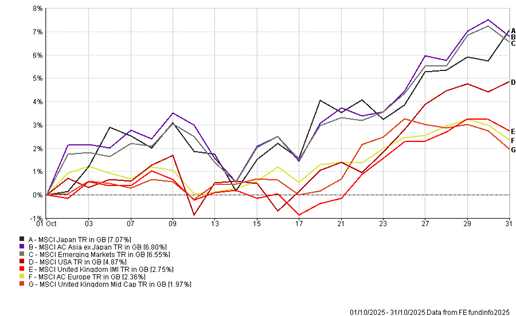

Japan: ‘The Takaichi Trade’

Japan elected Sanae Takaichi as its first female Prime Minister this month, which boosted markets given her pro-growth stance, promising fiscal stimulus, investment in AI and semiconductor sectors, and structural reforms. This triggered a wave of optimism among domestic and foreign investors, fuelling equity inflows. Japanese tech giants like Advantest and Tokyo Electron posted strong earnings and raised guidance, as investors piled into semiconductor and AI-related stocks, driving the Nikkei 225 up +15% its best monthly gain in 30 years. A softer yen improved competitiveness for exporters (autos, machinery), lifting earnings expectations and the continued accommodative stance from the BoJ supported risk appetite and equity valuations.

Equities: Earnings Improvement

Globally, US equities had a positive month, with strong earnings beats from mega-cap tech/AI companies such as Microsoft, Alphabet and Amazon. However, some names such as Meta had to remind investors of capex cycles ahead, given their less than expected earnings growth. As valuations rise, so do earnings expectations with the promise of investment in AI infrastructure continuing to fuel investor optimism for now.

In the UK, strong corporate earnings helped boost the FTSE 100 to all-time highs with pharmaceuticals (AstraZeneca and GSK) leading the charge posting positive Q3 results and optimism around drug pipelines. Financials, like HSBC and Barclays also posted robust earnings lifting sentiment. Gold prices climbed above $4,100/oz, boosting miners like Fresnillo and Randgold. These moves supported the FTSE’s commodity-heavy composition with energy and mining accounting for 25% of the index.

UK equities continue to remain cheap vs US peers, attracting global inflows amid AI-driven exuberance and institutional investors this year have added an extra layer of diversification to their portfolios as a form of geopolitical hedging.

US/China: Calm Before the Storm?

US China trade tensions dominated global headlines, swinging from escalation to a temporary truce. Early in the month, the United States threatened to impose 100% tariffs on Chinese imports, while China retaliated by expanding export controls on rare earth materials critical for semiconductors and EVs. Both sides also introduced new port fees and tightened technology restrictions, fuelling fears of a renewed trade war.

However, the tone shifted at the APEC Summit in Busan on October 30, where President Trump and President Xi agreed to a one-year trade truce. The deal included a tariff rollback (US average tariffs on Chinese goods cut from 57% to 47%), suspension of new rare earth export curbs, and a pledge by China to purchase 12 million metric tons of US soybeans in late 2025, with larger commitments for 2026–2028. The US also paused expansion of its export restrictions on Chinese tech affiliates, while China eased retaliatory measures on US chip firms.

Markets welcomed the truce, with Asian equities rallying and supply chain risk easing, especially for EV and electronics sectors. However, analysts warned that the agreement was tactical and structural issues like advanced semiconductor access and Taiwan remain unresolved, leaving the risk of renewed tensions in 2026.

Portfolio Changes

During the month, we have made one change across our OEIC funds with the introduction of the VanEck S&P Global Mining ETF. The fund provides exposure to a broad basket of precious metals and mineral based mining companies to benefit from the rise in prices and increased profit margins, adding further diversification to portfolios and inflation hedging. Within the Cautious and Balanced Funds this has come from a partial sale of Janus Henderson Strategic Bond and Ninety-One Diversified Income funds. For our Adventurous fund, we trimmed holdings in the Nomura Global Dynamic Bond and Castlebay UK Equity funds.

BOOLERS INVESTMENT COMMITTEE