Amandeep Mandair

Reveal Menu

Market Commentary: Monthly Bulletin September 2021

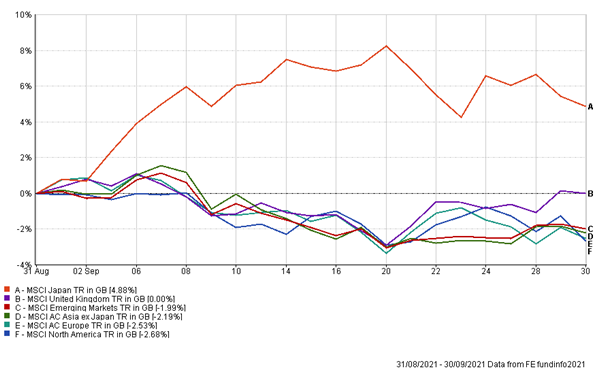

As we head towards the end of the third quarter of 2021, September saw some earlier years gains erased amid continued supply chain disruptions and rising inflation, despite this developed market indices remain on strong footing with growth stocks returning 12.2% and value returning 14.4% year-to-date. Performance of some of the main indices over the month are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

China took centre stage over the course of the month, as regulatory clampdown fears were exacerbated by the potential collapse of large Chinese property developer Evergrande. Although investors feared the potential implications this may have on the wider economy, the level of risk the property sector poses to the banking system appears manageable, abating systemic risks.

Across the pond in the US, investors awaited in anticipation for further news from Jerome Powell regarding the tapering timeline. The September meeting reiterated the view despite the effects of the Delta variant still lingering, tapering (slowing the pace of its asset purchases) is likely to commence as early as November, in preparation for a potential interest rate hike towards the end of 2022. The Bank of England also took a hawkish stance in its monetary policy, suggesting there may be an increase in interest rates before year end, however with quantitative easing still in full swing, the probability of an interest rate hike this year is unlikely. The ECB in comparison were slightly more dovish, as they stressed the process of tapering is not starting anytime soon, however, suggested some asset purchase reduction may take place.

Core Inflation continues to cause headwinds, as investors move to the idea that inflation isn’t as transitory, as first expected, the UK saw inflation reach a nine year high of 3.2%, up from the previous month’s 2%. Major prices hikes of commodities as well as the reopening of economies following the global pandemic have been the key reasons for rising inflation with the possibility these factors will abate over the coming months with inflation moving in line with market expectations.

Markets overall have been resilient to the wave of Covid hospitalisations, which have taken place over the course of the third quarter, with vaccine programmes still making headway across major economies. With winter approaching, Covid cases may cause short term headwinds to economic recovery causing some delays, however, we remain optimistic in the view that equities will continue to outperform fixed interest, which will is likely to continue into 2022.

The Boolers Investment Committee