Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin September 2023

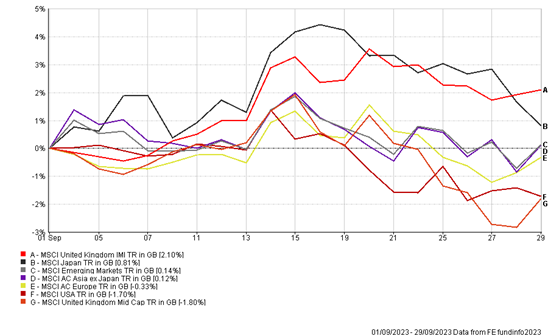

Markets were mixed over the month, as the higher oil price raised concerns that inflation could be harder for central banks to tame, meaning interest rates could remain higher for longer. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

As we have highlighted throughout the year, the main focus for markets remains inflation and expectations over how high and fast central banks will raise interest rates to bring this under control and back towards their targets.

Inflation generally has been on a downward trajectory during the year and monthly data points compare back to the same point last year. More recently, this has been brought back into focus as the oil price reached a 10-month high of $97 dollars a barrel in September (based on the international benchmark, Brent Crude Oil) due to additional supply cuts in production from Saudi Arabia and Russia. This will potentially lead to spikes in headline inflation and put more pressure on central banks to raise rates further or keep rates higher for longer.

Fixed Interest Securities/Bonds

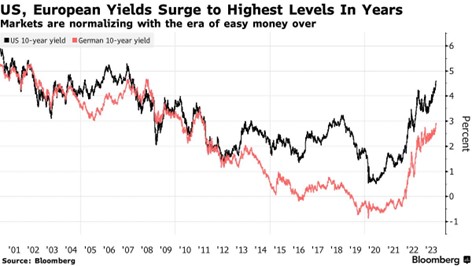

The chart below highlights US and European 10 year Government Bond yields over the last 20 years and whilst yields have risen sharply over the last two years, we are returning to a period of ‘normalisation’ relative to longer term rates/yields. Fixed interest as an asset class has struggled over the last two years as central banks have raised rates and as a result the capital value of bonds have fallen. We are close to the point at which rates will peak and fixed interest is now offering a more meaningful return in both income/yield terms and the potential for some capital upside, as and when rates reduce in the future.

UK Equities

In the UK, the Bank of England held interest rates at 5.25%, as members of the monetary policy committee voted 5-4 to leave borrowing rates unchanged. Better than expected inflation figures were announced before the meeting as the annual headline inflation rate fell to 6.7% despite the higher oil price and core inflation fell to 6.2% in August. The pause in rates led mortgage rates to fall, with prices continuing to decline since the summer, with deals being offered for new 5-year fixed rates below 5%.

Over the month, UK large cap companies outperformed due to oil majors being a large constituent of the FTSE 100 index and a weakening pound, helping to increase the revenues of international companies, with overseas revenues.

Global Equities

In the US, the Federal Reserve also left their interest rates unchanged at 5.25%, however they signalled that at least one more rate hike would take place this year and fewer rate cuts would take place in 2024 and 2025. The latest economic projections by the Federal Reserve have signalled that interest rates are likely to remain higher for longer because economic activity remains strong combined with a resilient labour market, despite job openings falling to lowest since March 2021.

In aftermath of the Federal Reserve’s meeting, the benchmark S&P 500, which consists of the highly valued so called ‘magnificent seven’ technology stocks, sold off as the higher for longer narrative pushed the 10-year US bond yield above 4.5%. Higher interest rates reduce the value of the earnings these ‘growth’ companies can generate in the future, based on their current share prices.

Japanese stocks continued to gain momentum in September, despite some profit taking towards the end of the month. Japanese stocks relative to other developed markets continue to look attractive on a valuation basis and have better fundamentals in terms of positive corporate governance reforms, supportive monetary policy and positive wage inflation, in a country which has suffered deflation for decades. We continue to remain overweight in Japan relative to our benchmark and increased our allocation to Japan earlier this year.

Asia and emerging markets had a subdued month, as investors assessed whether the Chinese government could take the necessary steps to address price deflation, high local government debt and fall in property prices. The Chinese government has already taken some action to boost incentives to encourage people to buy property, increase consumption and invest in the mainland stock market. There are signs that we may have reached peak pessimism, with latest figures showing industrial production increasing by 4.5% YoY and retail sales rising 4.6% and stronger manufacturing numbers in August.

Over the month, our underweight exposure to US and Europe equities and overweight positions in UK and Japanese equities have been positive contributors to performance. The third quarter has been relatively flat despite a volatile August and returns remain positive year to date.

THE BOOLERS INVESTMENT COMMITTEE