Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin October 2022

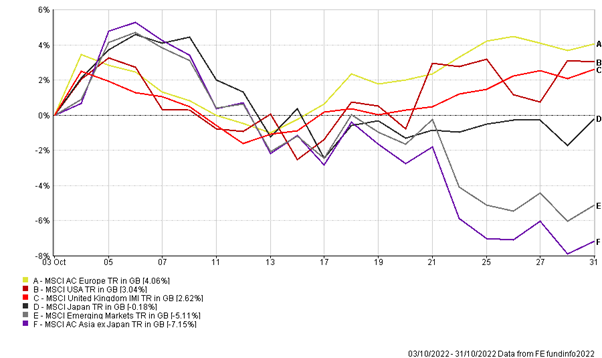

Markets were mixed for the month of October as investors reacted to the start of Q3 earnings season and speculation grew on where interest rates would likely peak in the US. The performances of the main indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

At the halfway stage of Q3 earnings season, 52% of S&P 500 companies have reported results so far, with 71% reporting positive Earnings Per Share (EPS) above estimates and 68% of S&P 500 companies have reported positive revenue surprises. The sectors leading positive earnings surprises have been Energy and Information Technology, but this was partially offset by negative earnings surprises in communication services, financials, and industrial sectors.

The better-than-expected earnings for Q3 come at a back of an annual US inflation rate of 8.2%, with core consumer prices rising for the month of September to 6.6%, compared to the previous month’s figure of 6.3%. The attention of investors will turn to the Federal Reserve’s upcoming meeting on 1-2 November, where investors expect the Federal Open Market Committee to agree to raise interest rates by 0.75% and traders have now made bets that the Federal Funds rate will reach 5% by May 2023 to combat sticky inflation.

A number of Federal Reserve officials have stated that to slow the pace of interest rate increases they need to see signs that inflation is beginning to fall on a month-on-month basis, in terms core inflation (which excludes food and energy), and service inflation, with prices meaningfully falling towards their long-term target of 2% inflation.

In the UK, September’s loser became October’s winner as Rishi Sunak became Prime Minster following the demise of Liz Truss’s ‘mini’ budget. The new PM has promised a new economic strategy that is focused on showing markets how debt as a percentage of GDP is likely to fall sustainably in the government’s autumn statement on the 17th of November.

However, before then, investors will turn their attention to the Bank of England (BOE) in their fight against inflation, which is now at a 40 year high at 10.1% as shown in the latest data for September. Financial markets are expecting the BOE to increase rates from its current level of 2.25% by 0.75% to 3%, which would be the largest increase since 1989. The size of the move in interest rates would be significant and would match the European Central Bank’s recent rise in interest rates by 0.75%.

The key consideration for the BOE is to what extent Sunak’s government is planning immediate tax and spending cuts which would help dampen inflationary pressures and weaken the need for large interest rate increases. On the other hand, if Sunak’s government has fiscal tightening earmarked for the next election in 2024, the BOE would be set on immediate action now to fight inflation.

In the Far East, as shown in the chart above, global investors reacted negatively to the re-election of President Xi’s third term as the General Secretary of the Communist Party of China (CPC). Xi effectively overhauled and took control of party leadership giving more power to his loyalists who are more concerned with the geo-political rivalry with the US rather than economic reform to help grow the Chinese economy. The selection of the leadership team creates worry for investors that Xi’s policies on the pandemic and national security will go unchallenged, even if it results in slower economic growth. This is shown in the latest data where China’s economy grew by 3.9% year on year in the third quarter, below the government’s 5.5% annual growth target.

However, despite the ongoing economic & geopolitical uncertainty, China still remains a major part of the global economy and they are seen as a growth engine for global growth. Therefore, Asian equities are currently trading at very attractive valuations and robust earnings growth is still to be expected going into 2023 and beyond. This could particularly be the case where investors anticipate the long-awaited re-opening of China’s economy, which would be a powerful catalyst for markets and a positive surprise would instantaneously result in a bullish response from global investors.

Our portfolios continue to be invested in equity and non-equity assets, diversified across different geographical regions, sectors and companies. We still believe equities will continue to outperform other asset classes over the medium to long-term, as company fundamentals remain intact.

As per our previous updates, we believe that long-term investors should stay fully invested and our blend of Value, Growth and Quality-oriented equity funds means that portfolios are well positioned to benefit from any style rotation and recovery in markets.

Over the month our risk models have moved broadly in line with markets, outperforming their respective benchmarks and peers, which has been a common trend thus far this year.

As always, should you wish to discuss your portfolio or markets more generally with your investment manager, then please do not hesitate to contact us.

THE BOOLERS INVESTMENT COMMITTEE