Simon Watts

Reveal Menu

Quarterly (and Half-Year) Market Update

Equity markets continued their gradual but positive progress over the second quarter, lifting portfolios further from their September lows. However, market positivity has to contend with the headwinds of inflation, recession fears and declining consumer and business confidence, hence the recovery in equity valuations is not across the board.

Bonds

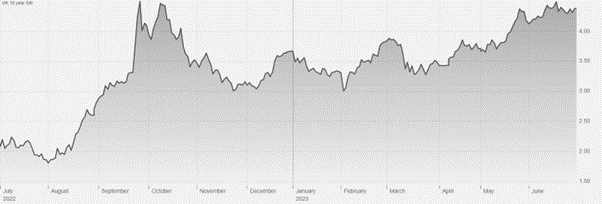

Bond valuations, which normally perform inversely to interest rate movements, have continued to fall as interest rates have risen and expectations for how high they will go have been revised upwards. As the chart below illustrates, 10-year gilt yields rose over the second quarter, returning to levels last seen during Kwasi Kwarteng’s Mini-Budget last September. Back then, the bond market was nervous about the cost to fund tax cuts and increased UK Government spending; now the concern is sticky UK inflation which requires higher interest rates, possibly for longer in order to tame it.

Chart: 10 Year Gilt Yields, July 2022 to July 2023

Source: Financial Times

Over the last quarter, the MSCI Markit Iboxx Gilts index fell by 6.0% and by 3.8% over the first half of 2023. As we sold all direct gilt exposure in the first half of last year, our bond exposure is mainly comprised of corporate and overseas sovereign debt. Whilst also not immune from rising interest rates here and elsewhere, the performance of our bond holdings has been between -1.0% and -4.8% over the quarter and between 0.7% and -4.8% year to date (the laggard being M&G Global Macro Bond which acts as an effective US Dollar hedge, during a period of a strengthening Sterling).

Interest Rates, Inflation & Currencies

With the usual exception of the Bank of Japan, Central Bank interest rates continued their march upwards, albeit mostly at a slower pace. The Bank of England base rate increased to 5% compared to 3.5% at the beginning of the year, increasing 0.5% in June. At the start of the year, we would have expected the UK rate to be at or near its peak by now at around 4.5%, but stickier than expected inflation figures mean that they may reach 5.5% to 6% and only start to reduce in the second half (or even final quarter) of 2024.

In the US, the Federal Reserve increased rates more hesitantly to 5.25% from 4.5% at the start of the year, whilst in the Eurozone, the European Central Bank increased rates to 4% from 3.5% at the start of 2023.

US inflation slowed to 4% with core (CPI) inflation at 5.3% in May, compared to figures of 7.1% and 6% respectively six months earlier. Euro Area inflation fell to 5.5% in June from 9.2% in December. However, the downwards trajectory for UK CPI inflation is shallower, standing at 8.7% in June from 10.7% in December. Most economists believe that inflation will eventually return to the Bank of England’s target rate of 2%, but they disagree over how long it is likely to take; in their latest Monetary Policy Report the Bank of England still appear to predict inflation returning to its 2% target around mid-2024. Currently, this fall is being held back largely by food prices and wage growth.

Chart: UK Consumer Price Inflation, 1989-2023

Source: ONS, via the ECO API

Year to date, Sterling continued to strengthen by 4.7%, 2.7% and 15.5% against the US Dollar, Euro and Japanese Yen respectively, weighing on Sterling-based investors’ returns on investments in these regions.

UK Equities

June was a poor month for market sentiment in UK equities (though Large Cap Value stocks recorded positive returns) and most of our UK holdings ended the quarter marginally in the red. However, it has been a more positive picture for UK equities year to date (with the exception of smaller companies), with most of our holdings returning between 2% to 5%, and the MSCI United Kingdom index is up 2.3% over this period.

In equity style terms, this has been a year of two quarters insofar as at the start of the year market optimism led Mid Cap and Growth stocks to outperform, whereas UK economic woes have led to a resurgence in the relative performance in Large Cap and Value stocks.

Whilst the UK economy faces significant challenges in the short and medium term, its equity market continues to trade on relatively attractive valuations, and we are confident in the ability of UK companies (many of which derive a significant portion of their earnings from overseas markets) to make positive progress from here.

Overseas Equities

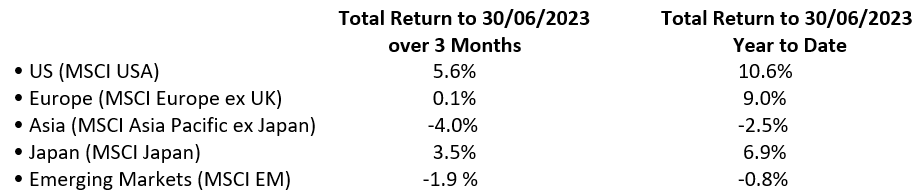

Index performances for overseas equity markets for the quarter to 30th June 2023 and year to date are shown below:

(All figures are based on bid-to-bid prices with income reinvested, in Sterling terms).

The stronger position of Sterling mentioned earlier is relevant here, as it masks stronger year to date performances in local currency terms, notably 23.8% in Japan and 5.6%/4.4% in Emerging Markets and the Asia Pacific region (excluding Japan).

The global equity benchmark (MSCI All-Country World Index ex-UK) returned 3.4% over the quarter and 7.4% year to date (13.9% in local currency terms). Of our global equity holdings, the Rathbone Global Opportunities fund continued to outperform the global equity benchmark in Sterling terms, returning 10.1%.

North America

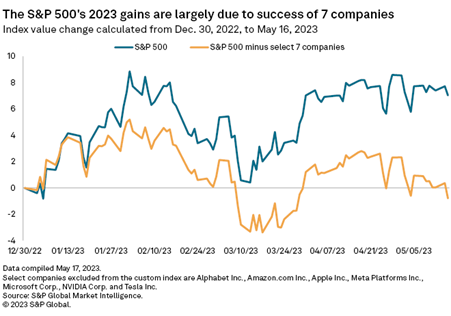

So far this year, the tech-heavy S&P 500 index has seen several of the more beaten up stocks (in 2022) recover spectacularly, namely the so-called ‘Magnificent Seven’ stocks (Nvidia, Tesla, Meta Platforms, Apple, Amazon, Microsoft and Alphabet) as investors made bets regarding the importance of Artificial Intelligence in the future.

The S&P 500 index has risen sharply (though is outdone by the Nasdaq, which has had it best first half of the year since 1983, after a very grim 2022), but this can be attributable largely to just seven stocks, as the following chart from Forbes illustrates:

This “narrow market” recovery may be of concern if it does not expand into a greater number of constituents, and we will be watching this closely in the coming months. The US are further along in the disinflationary cycle now playing out in Developed Economies, but economically speaking are not out of the woods yet. The full impact of interest rate increases to date has still yet to be fully felt in the economy, and fears remain that a slowdown in corporate earnings could give way to a recession later this year or in 2024.

Last year our combined US holdings outperformed the S&P 500 index due to the underperformance of this narrow range of stocks, so with our US equity allocation being weighted outside of them it would be logical to expect our holdings to underperform the iShares S&P 500 index tracker (core holding). Whilst this is true year to date, over the second quarter the Columbia Threadneedle US Smaller Companies fund’s performance matched the iShares tracker’s return of 5.7%, and in June it (along with Schroder US Mid Cap) outperformed the S&P 500, with JP Morgan US Equity Income close behind it, giving us some confidence that the US equity market recovery may indeed be broadening.

Europe

European equities were relatively muted in the second quarter after a strong start to the year, though our single European equity holding (BlackRock European Dynamic) eked out a return of 2.1% over the past three months and has returned 13% so far this year, well ahead of its MSCI benchmark.

European equity markets in the second half of the year will be heavily influenced by the European Central Bank’s stance (currently hawkish) on interest rates, which could dampen performance, and we will continue to monitor interest rates and inflation.

Japan

The Japanese equity market has gone through long periods of being out of favour with investors (as has the UK), but its performance year to date has justified our long term overweight position in this market. It is unsurprising that the already-weak Japanese Yen has lost further ground against major currencies whose Central Banks have embarked on rapid interest rate rises whilst the Bank of Japan has stood still, but this could also be regarded as a store of value for the future.

Over the quarter and year to date, the Value-oriented ManGLG Japan outperformed the MSCI Japan index, whilst the Growth-oriented Baillie Gifford Japanese fund underperformed, having produced an aggregate performance ahead of benchmark over the previous quarter and last year. We will be adding to our Japanese equity exposure over the coming weeks and reviewing our current holdings.

Asian & Emerging Markets

The Chinese reopening trade that was much vaunted coming into 2023 has thus far been disappointing, but they have loosened monetary policy at a time when other Central Banks are tightening and may go further. In addition, supply chain shifts away from China as a result from the pandemic will mean higher business and investment flows to other parts of Asian and Emerging market regions such as India, Vietnam, and Indonesia. These economies have more youthful demographics than the West, which will fuel consumption and a more energetic and productive workforce.

We continue to remain overweight in Asian and Emerging Markets against the benchmark because of attractive valuations when compared to Developed Markets, helping to diversify portfolios. Fundamentals in countries such as South Korea, India and Brazil remain strong, because these Central Banks were early in tightening monetary policy to curb inflation pressures.

Year to date our Asian and Emerging Markets equity holdings have outperformed their MSCI benchmarks by 1% to 2%, and we believe more generally that these markets will benefit from a further weakening of the US Dollar.

Portfolio Performance & Changes

Portfolio performances over the second quarter will have been mixed, with more equity-heavy Adventurous portfolios having the upper hand. However, virtually all portfolios should be in positive territory year to date, through a period that has had numerous challenges such as a mini US banking crisis, interest rate rises and high inflation.

As mentioned in a previous investment commentary, our investment priorities are split between allowing portfolios to benefit from future market recovery whilst trying to protect some of the gains made over the last few months, and our recent portfolio changes reflect this.

In June, we sold 1% from iShares S&P 500 ETF, taking some profits from the strong rally in technology and will be reinvesting these proceeds into iShares MSCI Japan IMI ETF, due to solid macro and domestic fundamentals in Japan.

We have also increased our cash weighting by an additional 5% in total. We have sold our total holding in the Artemis Global Income Unit Trust for all clients and, where tax allowances allow, we have also reduced our UK equity exposure by 2.5%, 1.5% and 1% proportionally across our risk models from Artemis Income Unit Trust, Columbia Threadneedle UK Equity Income OEIC and JO Hambro UK Equity Income OEIC. This is to provide some protection from the volatility in equity prices, as Central Banks keep interest rates higher for longer potentially pushing developed markets into a slowdown or (shallow?) recession.

Conclusion

The first half of this year has seen investment markets navigate choppy waters, but dire economic predictions have been repeatedly rowed back on. For example, the Bank of England no longer predicts a two-year recession in the UK, just as the International Monetary Fund withdrew its predictions of a UK recession this year and the weakest economic growth in the G7 group leading industrialised economies (barely a month after making it).

More widely, consumer spending and corporate earnings have recurrently outperformed expectations, avoiding (or at worst deferring) economic recessions. That said, we are still not at the end of the interest rate cycle and inflation is not yet under control or close to target rates.

Arguably the most important determinant of whether we see significant market recovery or recession from here is policy responses from governments and Central Banks. In the UK for example, the thrust of the response to curb inflation has been by the Bank of England at the demand end by raising interest rates to dampen spending. However, this encourages higher wage demands (inflationary) and inflation is stickiest around food, which there is a limit on how much we can reduce consumption of. With UK inflationary pressures being more at the supply end (primarily labour supply and food production), it is arguably government-led initiatives that are required.

Our view is that we will see economic recovery in the UK and elsewhere within the next year or so, but its pace and extent will be aided or impeded by the policy responses to controlling inflation, which need to be wide-ranging and targeted. The worst case scenario is that too much of the economic “medicine” (interest rate rises) causes harm and brings about recession, but we believe economic fundamentals are sound enough to preclude a significant downturn and remain confident that portfolios can make positive progress over the medium to long term.

THE BOOLERS INVESTMENT COMMITTEE