Simon Watts

Reveal Menu

Quarterly Market Update: April 2022

What a difference a day makes

Normally, we wait until the quarter-end performance figures are available before compiling our commentaries. However, due to pace at which events are developing in Ukraine, we thought it appropriate to provide our latest commentary at the earliest opportunity. Therefore we are providing this via email in advance of the normal valuations with all figures quoted up until 25th March.

As 2021 drew to a close, we looked forward to 2022 with guarded optimism. The Global Pandemic, which had weighed on markets for two years appeared to finally be in retreat, and the global economy was well on the way to reopening. Whilst we did not expect a repeat of the strong stockmarket growth of 2021 due to inflation concerns, we expected inflation to peak at around 6% during the first half of the year and falling back in the second half. However, Vladimir Vladimirovich Putin had ambitions that were detrimental to our cautious outlook.

24th February 2022 marked a paradigm shift in geopolitics: Russian armoured columns entered Ukraine from multiple directions, prompting us to provide an update to clients on the same day (available on our website). Over the course of the two weeks that followed, over 30 years’ worth of trading dependencies between Russia and the West were rolled back and a new Iron Curtain descended.

The humanitarian costs of Putin’s decision to invade Ukraine are huge; already we have seen the largest refugee crisis since the Indochina crisis of 1975, and the greatest in Europe since World War II. Civilian casualties mount daily, and the apparent indiscriminate shelling of Ukrainian cities are beginning to resemble the conflict in Syria. However, for the purpose of this investment commentary we will concentrate on the short and long term economic impacts of the conflict in Ukraine.

Put simply, the Ukraine conflict has amplified our expected economic challenges for 2022 – inflation will peak higher and later than expected, our concerns for inflationary impacts on consumer spending are increased and supply chains will continue to feature in our commentaries (though in different sectors than previously reported). That said, central banks and the International Monetary Fund, whilst acknowledging the risk of recession, have uniformly stated that this should not occur and still forecast positive (though reduced) economic growth for this year.

Bonds

10-year UK government bond yields started the year at nearly 1% and by 25th March had risen to 1.6%, their highest level since the first quarter of 2019. This means that gilt prices have fallen sharply year to date, with the MSCI Markit Iboxx Gilts index down 7.9% and the MSCI Markit Iboxx UK Gilt Inflation-Linked index down 6.3%.

Under “normal” circumstances this might indicate a “risk-on” period for investment markets, when investors shun safe haven assets such as government bonds in favour of riskier assets such as equities. However, this decline in gilt prices has much more to do with UK interest rate rises, and an inflationary outlook that suggests further rate rises will follow. Investment grade (blue chip) corporate bond prices have similarly suffered, with the MSCI Markit Iboxx Corporates index down 7.3% year to date.

Over the same period, the iShares Core UK Gilts tracker fund (held by Cautious and Balanced risk clients) fell 7.5%, whilst the M&G Global Macro Bond fund returned -2.8%, buoyed by a stronger US dollar. Our remaining corporate bond holdings returns ranged between -4.3% and -6.9%. Whilst in aggregate our bond holdings have outperformed their benchmarks relatively speaking, they have still fallen in absolute terms.

Interest Rates & Currencies

Interest rates remain unchanged again at near-zero levels in the Eurozone and Japan, but in the UK the base rate was increased by 0.25% twice (in February and March) and now stands at 0.75%, whilst in the US rates rose by 0.25% in March to 0.5%. The UK base rate has now returned to its level in early 2020 just prior to the Global Pandemic, whilst the US still has some way to go before it returns to its pre-pandemic level of 1.75%. European and Japanese rates have remained unchanged for several years.

Whilst the UK rate of 0.75% is low historically speaking (pre-Global Financial Crisis it was nearer 5%), further interest rate rises may follow over the coming months. End of year base rate expectations vary, as the Bank of England has a difficult balance to maintain of controlling inflation whilst not discouraging spending and growth. Some commentators have revised earlier expectations of 2% by the end of the year down to 1.25%, but the Office for Budget Responsibility (OBR) have speculated that it could reach 3.5% if businesses raise prices to maintain profits and employees receive real wage increases. We consider this scenario less likely and expect rates to be between the two lower estimates by the end of 2022.

In the US and the Eurozone, economic stability and labour markets are more influential on interest rate decisions, and the widely expected US 0.5% rate increase was pared back to 0.25% in March. Nevertheless, the Federal Reserve have warned that they are ready to act decisively if deemed necessary. The European Central Bank have stated that energy prices are largely responsible for pushing up inflation and interest rate rises will not change that fact.

UK CPI inflation reached 6.2%, its highest level since 1992. The Bank of England expect it to reach 8% by April and possibly double digits in the Autumn if there is another sharp rise in the energy cap. Inflation is already at 7.5% in the US and 5.9% in the Eurozone. However, the effectiveness of further interest rate increases is questionable when consumer spending is already under increasing pressure. Central banks must therefore avoid denting consumer confidence to the extent that they reduce or defer spending (which could lead to recession) whilst trying to reign in inflationary pressures exacerbated by external geopolitical factors – an unenviable task.

The US dollar has strengthened against major currencies year to date – 2.7%, 3.3% and 5.7% against Sterling, the Euro and Japanese Yen respectively. We attribute much of this to a general demand for US currency and assets during a period of heightened geopolitical tension; the Dollar could therefore weaken in the near future if the conflict in Ukraine comes to an end.

UK Equities

The MSCI United Kingdom index has gained 0.9%, due largely to its weighting in large cap stocks and oil and energy in particular.

Oil stocks enjoyed their best January in 30 years due to heightened demand from a global economy moving on from the Global Pandemic. Oil and energy stocks rose again sharply as the Ukraine conflict commenced, bringing into sharp focus the question of future global energy supply chains in the short term. Conversely, Small Cap and Growth stocks suffered during what has been a general risk-off period for investors, with larger companies with more predictable earnings/dividend streams being more in favour.

Consequently, fund holdings with greater oil and energy exposure, Large Cap and/or higher dividend paying stocks have fared better year to date. JO Hambro UK Equity Income and Artemis Income produced positive returns of 0.6% and 0.4%, whilst at the other extreme Liontrust UK Smaller Companies fell 15.4% and Marlborough UK Micro Cap (held by Adventurous risk clients only) fell 19.1%. It is worth remembering that these two funds have consistently and comfortably outperformed our other UK equity over the medium and long term and we remain confident in their ability to continue doing so over the longer term.

Overseas Equities

Index performances for overseas equity markets for the quarter and the year to 25th March 2022 are shown below:

(All figures are based on bid-to-bid prices with income reinvested, in Sterling terms).

The global equity benchmark (MSCI All-Country World Index ex-UK) returned -3.5% over the quarter and 12.6% for the year.

North America

As with the UK, oil, energy and commodity stocks outperformed along with other larger cap, higher dividend yielders. Technology stocks and smaller companies struggled but rebounded strongly in mid-March. The tech-oriented Nasdaq 100 index for example suffered its worst month since March 2020 in January, narrowly avoiding entering bear market territory (a fall of 20% or more) at the end of that month. Year to date the index is down 10.5%, but had fallen by 20.9% as at 14th March.

Year to date, the Large Cap, financials-weighted JP Morgan US Equity Income fund produced a benchmark-beating positive return of 1.2%, whilst the heavily US-weighted Polar Global Insurance fund produced a greater return of 5.7%. The core index holding iShares S&P 500 returned -2.3%, whilst the Threadneedle American Smaller Companies returned -4.3%.

We remain broadly positive towards the US equity market, which (like the UK) has a strong economy, low unemployment and Purchasing Managers Index numbers which despite current economic uncertainties still indicate future economic expansion. However, there is a growing consensus that the Federal Reserve is further behind the curve than the UK on tackling inflation, caused initially by looser monetary policy, which may require a more decisive response later in the year.

Europe

European equities sold off sharply, notably in Germany (who are heavily dependent on Russian gas) following the Russian invasion of a European neighbour.

Our single European holding (BlackRock European Dynamic) produced a rare underperformance, falling 15.7% due to its bias towards Growth stocks which were not in favour over the period. However, the fact that we are underweight in European equities within client portfolios, favouring UK equities instead (which have outperformed), the drag on relative performance here is limited.

Japan

The Japanese stockmarket has similarly been weighed down by inflationary concerns during the first quarter, but like many other markets appears to have digested the impact of the Ukraine conflict and recovered during recent weeks. As of 25th March, the Nikkei had risen for a ninth straight session, its longest winning streak since September 2019.

Over the quarter, the Value-oriented ManGLG Japan Core resumed its outperformance through negative trading conditions, returning 8.0% year to date, whilst the Baillie Gifford Japanese fund fell by 6.3%, producing an aggregate performance ahead of benchmark.

Asian & Emerging Markets

Asian and Emerging Markets surfaced from a year of poor performance into an economic climate that in some ways could be regarded as decidedly hostile.

China, still grappling with COVID-19 and locking down entire cities to contain the spread of the virus, has to deal not only with the resulting economic fallout but also with supply chain constraints, is now having to carefully negotiate a difficult diplomatic middle ground between Russia and the West. The greater and more complex trading relationships China enjoys with the West compared to Russia will hopefully prevent economic sanctions being imposed on them. Whilst China has signed a major energy deal with Russia which undoubtedly supports them economically, it is hoped that the much greater economic ties with the West will limit their support for Russia diplomatically and militarily.

The positive factors for investors in China include their capacity to stimulate their economy, having not cut interest rates throughout the Global Pandemic. President Xi’s “re-election” at the Chinese Communist Party Congress, expected to place around November this year, incentivises such stimulus and arguably disincentivises China from adding to geopolitical tensions or incurring economic isolation in the short term.

India has enjoyed a very strong period of economic growth, though like China has been openly criticised for not condemning Russia’s actions in Ukraine. As Russia has been their primary fertiliser and arms supplier since the Cold War, it is difficult for India to turn their back on them, particularly considering the agriculture sector is one of the most important industries in their economy and ongoing border tensions with China perpetuates their military spending. Though not as dependent on export markets in the West as China (and so perhaps better insulated from Western sanctions), India will nevertheless suffer disproportionately from inflation in global fertiliser and oil prices, even though they are currently acquiring both at discounts from Russia.

Russia, deemed an emerging market just two months ago, is now practically uninvestable. Not only has the Rouble collapsed against major currencies, their stockmarket was suspended just after hostilities in Ukraine commenced, having plummeted on 24th February. Our exposure to Russia within portfolios was always minimal, and we sold client holdings in the UBS Emerging Market Equities fund which had a very small weighting just prior to the Moscow stockmarket suspension.

Latin America as a region is likely to benefit as a major commodities producer from the sanctions on Russian trade, and regional equity market performance has been very strong year to date. As emerging market funds reposition themselves following recent events, it is likely they will tilt more in the direction of this region.

At fund level, the Schroder Asian Alpha Plus and First Sentient Asia Pacific Leaders Sustainability funds have fallen 5.7% and 9.8% year to date, whilst our remaining emerging market fund managed by Fidelity has fallen 15.4% Clearly, this has been a very challenging period for Asian and emerging markets, but we believe these markets have strong upside potential over the medium term.

Portfolio Performance/Portfolio Changes

Portfolios will have experienced their first negative quarter in two years, typically contracting between 5% to 6% depending on the portfolio’s risk level. Ethically-focused portfolios will have fallen by between 8% to 9%, due to their lack of exposure to fossil fuels and Value stocks. Whilst this is disappointing, the vast majority of portfolios will still be in positive territory over 12 months, and for clients who have been invested for more than two years, their portfolios should be well ahead of where they were at the market peak before the Global Pandemic.

We have made several changes to portfolios so far this year:

Clearly, we will be monitoring the ongoing situation in Ukraine closely and make any changes deemed necessary insofar as they relate to portfolio holdings.

Don’t Feed the Bear

A namesake and predecessor of President Putin, Vladimir Ilyich Ulyanov (aka Lenin) once said: “There are decades when nothing happens, and there are weeks where decades happen”. Since the fall of the Soviet Union in 1991, the West has increased its dependency on Russian oil and gas (though the latter continued to be piped into Europe uninterrupted throughout the Cold War) and in turn has exported to Russia seemingly every western brand from McDonalds to M&S. Russian oligarchs who emerged in the post-Soviet era were able to spend and invest their new-found wealth in the West (and in London in particular).

In a matter of weeks much of the above has been reversed, with assets frozen, yachts impounded, and diplomats expelled. Gas still flows into Europe through Ukraine via Nord Stream I, but Nord Stream II has been shelved indefinitely. The number of economic sanctions imposed on the Russian State and key individuals dwarfs those imposed on Iran. NATO is united in its opposition to the Russian invasion and countries outside of the alliance such as Japan and Australia have been vocal in their condemnation of Putin.

The strategy of punitive sanctions is to strangle Russia economically and impede its ability to finance a long term war with Ukraine. China and India have thus far resisted taking sides and have actually increased purchases of oil and gas at discounted prices, good for their economies but also providing Russia with an economic lifeline.

We do not believe relations between Russia and the West will return to their previous levels for many years due to the mutual distrust that now exists, nor do we believe there is a short term solution to the Ukraine conflict that would benefit both sides enough to accept it. Like Afghanistan or Iraq, we could be in for an extended period of military occupation in Ukraine (though we hope we are wrong).

Although Russia’s stockmarket has reopened for trading in a limited number of stocks, the last time it was suspended for this length of time was 1914; after reopening briefly in 1915 it remained closed for over 75 years.

So how should we view the unfolding situation from an investment point of view? We know that markets hate uncertainty. The scale of economic sanctions imposed by the West severely impacts Russia’s participation in global trade, sporting events and even the Eurovision Song Contest. In so doing, the West has created for itself an oil and energy supply shock that cannot be solved overnight, and Russia’s invasion of Ukraine could cause a global shortage of corn, wheat and vegetable oils. Added to an environment of already-elevated inflation and on the face of it the economic outlook looks very uncertain indeed.

Yet faced with such uncertainties markets find a way, just as they did through over 45 years of the Cold War. It is in some ways a sad reality that over time markets adjust to the new reality of conflict and move on. In our 24th February update we cited various examples of conflicts and how markets, after initially falling sharply, went on to recover strongly.

The very fact that many conflicts over the last fifty years have involved oil producing regions such as Kuwait and Iraq (and now Russia and Ukraine) means that energy and commodity prices tend to rise. This keeps inflation relatively elevated because higher energy prices offset reduced consumer spending and therefore wider economic growth.

One potential outcome being talked about now is ‘stagflation’, whereby inflation remains high, unemployment increases and economic growth remains low. However, as inflation eventually reduces (possibly with the aid of economic stimulus) the economic environment becomes more business and consumer friendly and markets respond positively. In late March, Christine Lagarde (President of the European Central Bank) said that she did not consider it likely that stagflation would take hold in the Eurozone.

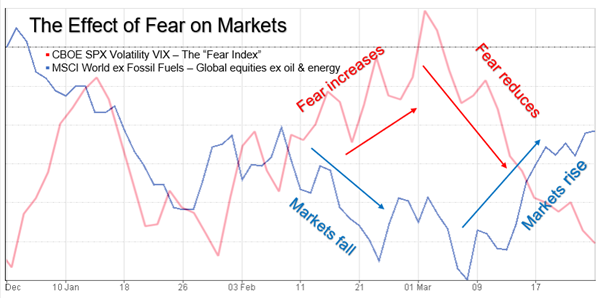

Markets may already have begun to adjust to the new geopolitical reality. The Chicago Board Options Exchange’s Volatility Index, more popularly known as the “Fear Index” or simply the “VIX”, began to rise in early February to levels not seen since the worst of the Global Pandemic, but from the second week of March began to fall again. Within days of the VIX passing its peak, equity markets (and particularly the sectors most beaten up in the preceding weeks), began to recover sharply to pre-conflict levels. The chart below illustrates the inverse relationship between fear and market prices in the shorter term.

In several ways we believe the Ukraine conflict will do more to shape global trade than the Global Pandemic, which along with the Global Financial Crisis and Brexit will be remembered by the investment managers at Boolers for years to come. However, wars invariably end in negotiation and (if previous armed conflicts are anything to go by) markets will respond positively.

Whilst the Ukraine conflict is still in its early stages, and the economic difficulties it will present to the wider world are still to be fully realised, we do believe that longer term investors will be rewarded for their patience during these volatile markets, and in the meantime, we will strive to make any changes we deem necessary to adapt to the ever-changing geopolitical landscape.