Sam Hubbert

Reveal Menu

Revealed: What the Bank of England base rate rise means for your finances

The Bank of England (BoE) has announced a rise to its base rate, up to 0.75% from the historic lows it sunk to at the onset of the coronavirus pandemic.

The recent increase (17 March 2022) marks the Bank’s third rate rise since December and reinstates interest to pre-pandemic levels. The rise also marks the first time in more than 20 years that the BoE has increased the base rate at three successive meetings.

The BoE used the announcement to confirm that rising inflation was partly responsible for their decision. It could be set to rise higher than it had previously forecast, partly in response to the war in Ukraine.

Russia’s invasion of Ukraine, it said, could see inflation peak “several percentage points higher” than its initial 7% forecasts, potentially at around 10%.

Keep reading to find out what the most recent rise means for you and your finances, and what the rest of 2022 could hold.

One role of the Bank of England is to keep inflation in check

The BoE has historically used interest rates as a means to control inflation.

When interest rates are low, cash savings generate little interest, encouraging savers to spend it instead. This leads to rising inflation. Conversely, when interest rates are high, inflation tends to fall as people save, rather than spend, their hard-earned cash.

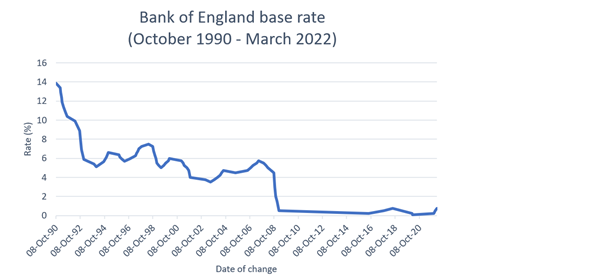

The onset of the coronavirus pandemic in March 2020 created stock market volatility, increased government borrowing, and slowed the UK economy. GDP dropped to its lowest level since records began and the BoE dropped its base rate to a historic low of 0.1%.

This cut was designed to encourage consumer spending and thereby stimulate the economy.

Data source: Bank of England

As lockdowns lifted in the summer of 2021, however, a pent-up desire to spend – coupled with global supply shortages and rising fuel prices – saw inflation increase rapidly.

Back in May 2021, the BBC reported a doubling of inflation to April, rising from 0.7% in March to 1.5% a month later. By June, the BoE was reporting that inflation had exceeded its 2% target. It has continued to rise since and is set to peak at around 10%.

Interest rates returning to pre-pandemic levels might have a small effect on inflation, but the rise could have a larger impact on your finances.

What does the interest rate rise mean for your financial plans?

Savers have faced uncompetitive interest rates since the 2008 global financial crisis. In this context, any rise is to be welcomed.

However, an increase of just 0.25% might not make a great difference to cash savings. For one, there is no guarantee that your high street bank will pass the interest rate rise onto you. If they do plan to do so, it might take a while for the rise to filter through.

Also, with inflation set to continue rising, you’ll probably find that your interest rate remains a long way behind inflation. When the growth of your cash savings fails to keep pace with inflation, your money is effectively losing value in real terms. This problem looks set to continue.

The base rate rise could also increase your mortgage repayments if you’re on a variable- or tracker-rate product, further squeezing your finances.

Professional financial planning can help

With inflation set to increase over the coming months, and the potential for it to stay above the BoE’s target of 2% until 2024, you might find you need to keep a tighter rein on your budget in the short term.

Your long-term financial plan, however, is designed for the long haul, specifically to weather short-term economic unrest. If your goals haven’t changed, it’s unlikely your plan will need to change either.

Be sure you have an emergency fund in place but limit it to between three and six months of household spending. Holding too much in cash could see your money lose real-terms value when measured against inflation.

If you have excess cash, you might consider using it to top up your investments. Despite short-term market volatility, the potential for inflation-beating returns – albeit with added risk – could see your wealth grow in line with the general upward trend of the markets. You’ll need to have a long-term goal in mind though, and be sure you understand your risk profile.

At Boolers, we can help you put together a financial plan that considers the whole economy and focuses on your long-term goals. We’ll then schedule regular reviews to give you peace of mind that your plans remain on track and that your goals are still attainable.

Get in touch

If you would like to discuss the recent base rate rise or how Boolers can help you with any aspect of your long-term financial plans, please contact us today.

Please note

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.