Gavin O’Neill

Reveal Menu

The Benefits of Active Management and Compounding Dividends

2018 has seen the return of the dreaded ‘V’’ word – volatility. Since the beginning of February, investors have been concerned with how interest rates will rise over this year and beyond in comparison to previous expectations. Combined with this, US rhetoric is becoming increasingly more aggressive around protectionism and imposing trade tariffs.

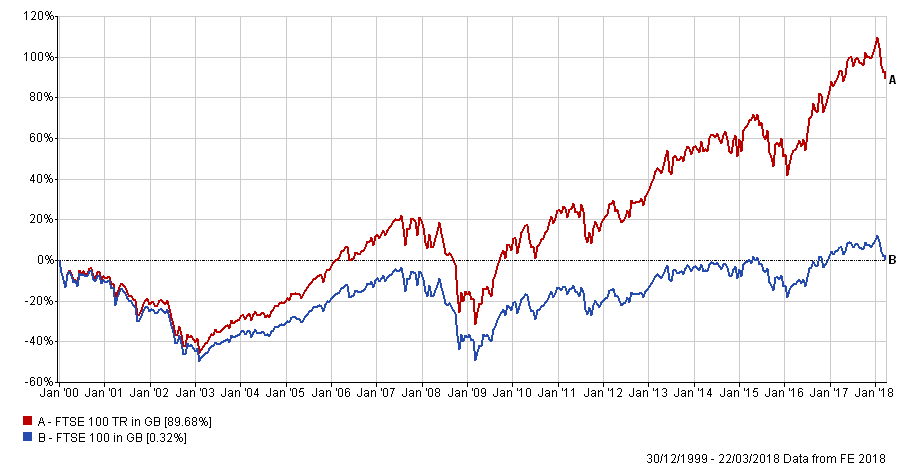

Within the UK, the FTSE 100 Index, has at the time of writing, moved below 7,000 and whilst this is much higher than the low points reached in January 2003 and January 2009, is back to the same level as the high point reached at the end of 1999 – the height of the ‘tech boom’.

There are two points that we would highlight here. The first is the power of compounding dividends over the longer term. Investment styles come in and out of fashion and it is fair to say that growth and momentum have been leading the way in more recent times. Within our portfolios we blend different styles of management to add valuable diversification and risk management. More traditional value stocks have lagged of late, however, the strong dividend culture within the UK should not be ignored and can be a significant contributor to returns over the longer term. The chart below shows the performance of the FTSE 100 from January 2000 through to March 2018, both in capital terms and with income yield reinvested – a difference in return of some 90%!

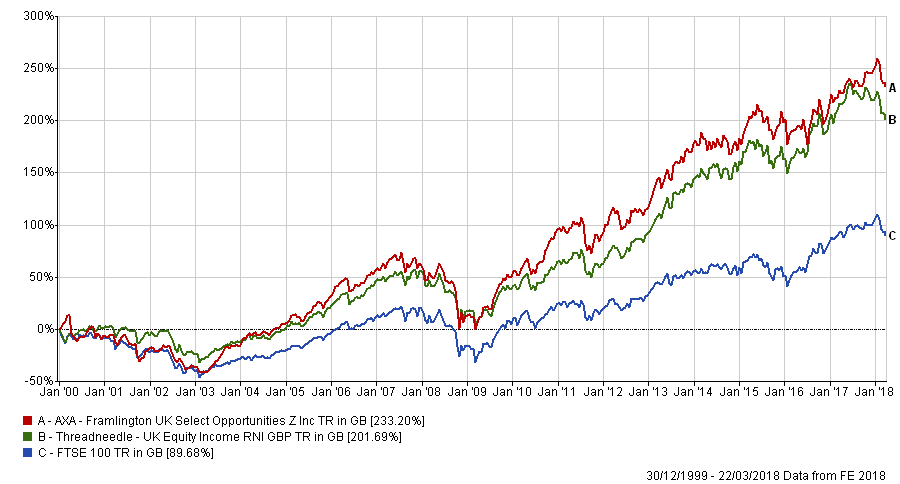

Taking this a stage further, we have and continue to favour active management within our portfolios in the belief that good quality fund managers can outperform indices and passive strategies over the longer term and through changing market cycles.

The best way to illustrate this is to highlight the strong outperformance of two active managers, one income orientated and one more growth focused, that we have invested with over the last two decades and continue to do so.

The chart below compares the Threadneedle UK Equity Income and Axa Framlington UK Select Opportunities funds with the FTSE 100 Index over the same period as the previous chart, i.e. since the beginning of 2000. These figures are based on the total return (income reinvested), although the capital only returns deliver an equally strong message with returns of 48% (Threadneedle) and 164% (Axa), compared to the index which is completely flat. Clearly in this example, a passive investment strategy would have only tracked the index after accounting for management fees and provides no opportunity for over (or under) performance.

We do expect that volatility will be present for some time and whilst we may see further bouts of weakness, we continue to believe that equities are well placed to provide competitive returns over the long term relative to other asset classes, especially when factoring in the benefits of compounding dividends and active management.

If you are interested in learning more about Active Management, call us on 0116 240 7070 or email enquiries@boolers.co.uk.