Simon Watts

Reveal Menu

Trump’s Tariffs and the Implications for Investment Markets

On Wednesday, Donald Trump announced wide-ranging tariffs against imported goods from much of the rest of the world.

Whilst these have been signposted for weeks, the level of tariffs imposed on the European Union and the UK were either as anticipated or even not as high as feared. Asia, however, were disproportionately targeted, sparking fears of retaliation from the world’s largest producer of goods (China) and the world’s largest consumer (the US) and the prospect of a global trade war.

As a result, global stockmarkets fell sharply on Thursday as they absorbed the impact of Trump’s announcement, and again on Friday as China announced retaliatory measures.

The purpose of this update is to (a) explain the background to Trump’s tariffs move, (b) summarise how global investment markets have reacted and why, and (c) outline how things could play out from here.

At the outset, however, we would stress that although the extent of these tariffs are unlike anything we have seen before, their impact on financial markets is familiar – we have experienced it 3 times in the past 7 years to different degrees, and on every occasion markets recovered in full in the short term. We will therefore set out the case for markets to recover again.

Background

For many years, Trump has held a firm conviction that many countries (but especially China) have been “ripping off” America, exporting their goods to the US with low tariffs whilst applying heavy taxes or even banning US imports. He reserves particular ire for Europe, who he describes as “friendly countries” that take advantage of the US, both through trade and their under-investment in the NATO defence partnership.

In Trump’s mind (and with some justification), cheap imports have undermined US industrial production. Therefore, to address this, he simply needs to level the playing field and factories and jobs can return to the US, making America great (and wealthy) again.

Trump imposed tariffs during his first presidential term, but on a smaller scale than now proposed; 25% and 10% on steel and aluminium in January 2018, and later that year threatened to go much further, causing markets to fall sharply in the final quarter of 2018.

Rather than concentrate on the case for or against this view, it is important to note that Trump’s focus is not so much on the rates of tariffs imposed, but rather the trade deficit between the US and other countries.

What Are Tariffs?

Tariffs are taxes imposed on goods that are imported from other countries, essentially increasing the price of those goods for consumers or businesses. So, for example, a Chinese exporter does not pay a US import tariff, though the cost of it may be shared between the US consumer and the US importer, who may in turn demand a lower price from the Chinese supplier.

Trump’s Proposed Tariffs

The tariffs announced on Wednesday start with a “baseline” tariff of 10% on virtually all goods imported into the US, effective from 5th April 2025. Then from 9th April, 57 countries will face higher “reciprocal tariffs”. Many nations, such as the UK, Brazil and Singapore, will face nothing above the 10% baseline, but others will face higher levels, with the EU being set a total tariff of 20% and China 34%.

In the run up to the announcement, we were led to believe that US tariffs would be based on an in-depth assessment of tariffs, value taxes and other barriers to trade imposed by other countries on the US – in other words, equal reciprocal tariff levels. However, the new tariffs have been calculated by taking the US trade deficit with each country, dividing it by total US imports from that country, then halving the resulting ratio and converting it into a percentage – in other words, based on trade deficits, not reciprocation.

This has led to some unusual outcomes, with the US applying a 73% tariff on the French island of Réunion, but only 10% on Mayotte and Martinique. Canada and Mexico were excluded as they have already been targeted in previous tariffs, Russia because trade with them is effectively sanctioned, and North Korea, Cuba and Belarus were excluded because existing tariffs and sanctions on them were already so high.

How Have Markets Reacted?

On Thursday, the US S&P 500 index fell by 4.8% (and over 10% since Trump took office, marking the worst 10-week start under a new president since George Bush came into power in 2001). On Friday, China hit back at the US with a reciprocal 34% levy on all American-made products, and the S&P 500 index fell by a further 6%, the highest fall since the Pandemic, reaching the lowest levels since May 2024.

In the UK, the FTSE 100 fell by 1.6% on Thursday and by 5% on Friday. Over the week, the US was down about 8.7%, UK 7.4%, European markets somewhere in between, with only China relatively unscathed at -0.3%.

Markets in Asia fell in early trading on Monday, and as of 7am, European and US stockmarkets were down pre-market.

Companies that have suffered the most understandably include those who stand to suffer disproportionately from these measures, examples being Apple, a US company whose products are widely sold in the US but are assembled in China, and Tesla, a US company whose sales were already plummeting in Europe and elsewhere, but who still enjoyed healthy sales revenues in China.

Most equity (share) markets are in the red over 6 months, though UK Government and quality (investment grade) corporate debt were slightly positive for the week.

Why Have Markets Reacted So Strongly?

The short answer is uncertainty – markets hate it; Trump has fundamentally disrupted global trade in a manner that was not fully anticipated, the consequences are as yet unknown, and what we know already doesn’t look good. So far, we have only seen the downside, and markets are only considering further bad news, without factoring in any positive resolution.

In the short term, markets often overreact to a short term shock (the “fight-or-flight” instinct) before calmly reassessing the situation and thinking forward. What occurred this week is just another example of that.

The American economist, Larry Summers, described Trump’s tariffs announcement as a Supply Shock, and we believe this is exactly how they should be viewed.

As stated, whilst we’ve not seen these levels of tariffs imposed since the 1930s, we have seen supply shocks twice in the past 5 years. In 2022, Russia invaded Ukraine, and from an economic point of view the Russo-European trade in oil and gas, which had been relied on for decades, was unexpectedly fractured. This impacted the UK and Europe more directly, but as the US were more self-reliant and Asia continued to purchase Russian oil and gas, the impact of this supply shock was relatively contained.

A far bigger supply shock was felt in 2020, when the Pandemic saw lockdowns imposed and half of the world’s industrial production was brought to a halt for several months.

In both instances, stockmarkets fell sharply, though in 2022 the situation was exacerbated by the rapid rise in inflation, caused partly by a further supply shock of huge economic stimulus in response to the Pandemic shutdowns. Also, in both instances, there were winners and losers – Amazon and other tech stocks won in 2020 as we had to stay indoors (and oil lost as we didn’t go anywhere), whilst in early 2022, oil and fossil fuels were the big winners due to the increase in industrial production and sanctions against Russia (whilst tech stocks were the losers as interest rate rises decimated their optimistic share price valuations).

How Long Did It Take Stockmarkets to Recover From These Supply Shocks?

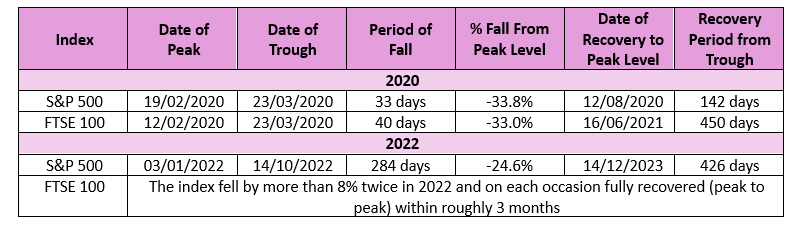

Not very long – in the table below we’ve shown the extent of the falls, or “peak to trough” and how long it took to regain those peak levels, using the tech-heavy S&P 500 and fossil fuel-heavy FTSE 100 indices:

In 2020, the S&P 500 index fell by a third in just 33 days then took a further 142 days to recover to it’s original level – less than 6 months – whereas the FTSE 100 took around 16 months to achieve the same feat.

2022 was a drawn-out period of rising inflation and economic woes which saw the US index decline over a period of over 9 months and take a further 14 months to fully recover, whilst the FTSE 100 bounced around but ultimately kept recovering and finished the year in positive territory. Even then, the US woes were not as keenly felt by UK investors, as a stronger dollar saw the S&P 500 firmly in recovery territory by July 2023.

How Are Stockmarkets Likely to Perform From Here?

From a “market certainty” point of view, we are still only in the early stages of the big reveal – Trump showed his hand on Wednesday, China showed theirs on Friday, whilst the EU and others are still formulating their response. Behind closed doors, there will be frantic negotiations taking place between the US and the rest of the world, and only after these have been completed will markets know what the new framework for global trade will look like.

As of yesterday, markets appear to be taking a cautious, perhaps pessimistic point of view based on what they don’t know. They are mindful that without some sort of resolution a US-led global recession becomes more likely. Even before the tariffs were announced, speculation about their likely impact had already caused businesses to pause investment and recruitment, which is being reflected in some of the latest economic data. Right now, we are at such a crossroads of uncertainty it almost feels like a “bad certainty” might be preferable for markets to at least regain some forward direction.

The best-case scenario is that the reciprocal (above baseline) tariffs are a bargaining position from which Trump is willing to compromise in exchange for concessions – this could enable a faster recovery of markets in the short term by way of a relief rally.

The worst case is that non-US countries all retaliate with reciprocal tariffs that nobody budges from – this will seriously damage the free flow of global goods, affecting supply chains, increasing costs to consumers and embedding higher inflation and lower economic growth into the system for years to come. Even in this scenario, however, there are positives as closer economic ties would likely emerge between Asia and Europe and, from an investment point of view, certain sectors will be winners or losers as we have seen in the past. Countries with lower reliance on US exports will also not be as badly affected.

The biggest lesson investors have learnt from previous supply shocks, however, is not to jump ship and to hold on for the recovery – exiting the market after such sharp falls crystallises losses that can only be recovered if you time your re-entry perfectly to benefit from market recovery, which can only really be judged in retrospect.

Boolers’ Investment Committee are following these events very closely indeed and will consider with each development whether its impact is temporary or indeed structural, which might require a change in emphasis in the blend of investments held within the portfolio. We may provide further commentary should we feel circumstances warrant it.

Clients taking “natural” income from their investments (dividends and interest) should continue to do so, however, those who are taking fixed withdrawals might wish to consider suspending them for a period, whilst markets work through the current volatility and recover. Conversely, clients holding excess cash may wish to consider whether this might be a good entry point for capital growth (however, we would still advocate that equity-based investment should be carried out with a timeframe of 5 years plus).

For now, we feel vindicated in our stance of not getting carried away with the “Magnificent 7” stocks in the US (Apple, Microsoft, Google parent Alphabet, Amazon.com, Nvidia, Meta Platforms and Tesla) and have maintained an overweight position in UK equities, which from a valuation and sector perspective are especially compelling now.

As always, if you have concerns and wish to discuss the current situation in further detail, please feel free to contact us.

Boolers Investment Committee