John Allen

Reveal Menu

Understanding long-term investment – Capacity for loss versus attitude to risk

Following a decade of low saving’s rates in the wake of the global financial crisis, the coronavirus pandemic hit the UK economy and saw rates dip to historic lows.

Even as the Bank of England confirmed recently that it would keep its base rate at 0.1%, it also forecasts that inflation could rise above 4% – twice as high as its own target of just 2%.

In this economic environment, money held in cash accounts with poor rates of interest will be unable to keep pace with inflation, meaning that your money is effectively losing value in real terms.

Turning to investments might offer a way to make inflation-beating returns but it comes with additional risk too. Invested funds can rise as well as fall, but with the value of your cash savings effectively dropping, the biggest risk to your financial future could be failing to take any investment risk.

That means understanding your risk profile, your capacity for loss, and the difference between the two.

Keep reading to find out why investing might be the right option for you and how Boolers can help you understand some of the key concepts of investing.

The benefits of long-term investment

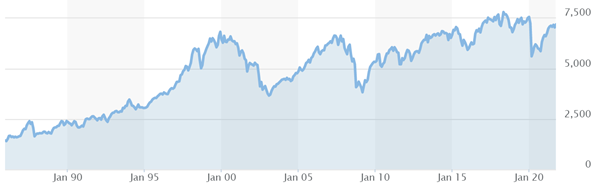

Here’s the FTSE 100 Index since 1986:

Source: MarketWatch

Despite clear dips including the 2008 financial crisis and the more recent impact of the coronavirus pandemic, the general trend of the market over the last three decades has been upward.

This is the reason we recommend that investments are made with a long-term goal in mind. A longer investment term means that your fund has more time to grow but also more time to recover should a short-term downturn cause the value of your funds to drop.

A shorter investment period, on the other hand, runs the risk of dipping at the exact moment you need to access the funds, and this could force you to withdraw your money at a loss.

The role of diversification and asset allocation

In a bid to avoid losses of this kind, and to enable you to benefit from the highest possible returns for the lowest possible risk, we can manage your asset allocation and diversify your portfolio.

Diversifying across asset classes, sectors, and locations spreads your investment risk. This is because a fall in any one area – a particular share or country – will hopefully be offset by a rise in another area. Your portfolio will also consider your attitude to risk and your capacity for loss.

Attitude to risk versus capacity for loss

Before you begin investing, you’ll need to think about your attitude to risk. Many factors will influence this, including what your long-term goals is, how far in the future it is, and your general attitudes to money.

Generally, you can afford to take a greater risk over a longer term, but your goal will impact your risk profile too. Your attitude to risk in your own retirement fund might be different to a fund you are saving for your child’s higher education, for example.

Your capacity for loss, on the other hand, is your ability to absorb a fall in the value of your investment without your standard of living being affected.

We can help you understand your capacity for loss. We’ll do this by looking at your incomings and outgoings, and by breaking down your expenditure into three categories:

By understanding your current finances – and the potential of those finances in the future – within the context of these three expenditure levels, we can calculate your capacity for loss. We will then use this calculation to inform our discussions about the right level of risk for you.

Your knowledge and experience (and the importance of remembering that everyone has to start somewhere)

The plan we put in place for you is as individual as you are. That means we must take your financial circumstances into account, but also acknowledge your level of experience.

As we’ve seen, with interest rates low and inflation high, now is a great time to start investing (if it’s right for you).

You might be concerned that a lack of knowledge makes investment riskier but remember that everyone has to start somewhere, and we will be there for you every step of the way. We can provide as much or as little advice and steering as you need, helping you to achieve your investment goals.

Get in touch

Boolers can help you manage your investments whether you’re a stock market expert or a novice so please contact us today for help with building or managing your portfolio.

Please note

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.