Simon Woodhead

Reveal Menu

What rising interest rates really mean for your clients’ savings and Investments

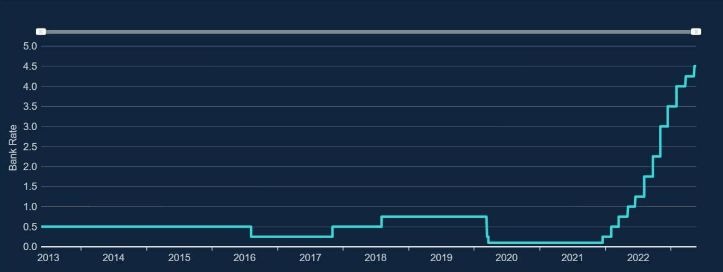

On 11 May 2023, the Bank of England (BoE) opted to increase its base rate.

The rise was decided at a regular meeting of the Monetary Policy Committee (MPC), which opted to increase the rate for the 12th consecutive time since December 2021.

Source: Bank of England

Before the December rise to 0.25%, it had stood at just 0.1%. Now, following the most recent increase, the base rate is 4.5%.

What does this mean for your clients’ savings and investments?

Keep reading to find out.

Rates are rising, but inflation is still high and falling slowly

With rates rising, your clients might be putting increasing faith in their cash savings, but this could be premature.

Times have been tough for savers dating back to the global financial crisis of 2008. And while the BoE’s base rate rise might be passed onto savers in some instances, the best available rate on an instant access savings account according to Money Saving Expert was 4.25% (as of 23 May 2023).

This is 0.25% below the base rate. More importantly, though, it’s half the current rate of inflation.

The Office for National Statistics (ONS) confirms that the Consumer Prices Index (CPI) for the 12 months to March 2023 is 10.1%. While inflation is falling, it is doing so from a 41-year peak of 11.1% in October 2022. And it’s falling slowly.

In fact, inflation isn’t expected to return to the BoE’s 2% target until late 2024.

Your clients will need to think twice before holding too much in cash

With bank interest rates still well below current inflation, your clients will need to think carefully about the amount of money they hold in cash.

Maintaining an emergency fund – ideally equal to around three to six months of household expenditure – is key. But holding too much could be a bad idea.

While interest rates remain below inflation, money held in cash is effectively losing value in real terms as its buying power diminishes.

This means that holding enough for a “rainy day” is a slightly more difficult juggling act. Your clients will need to keep on top of their fund to ensure it maintains its real terms value without committing too much to an account that is effectively losing value.

Investing could offer the chance of inflation-beating returns

In the same way that poor savings rates tempt savers to invest, some timid or reluctant investors might see rising rates as a tempting reason to hold excess savings in cash.

While investing carries an element of risk, weighing up a few simple factors could help your clients to decide if investing is right for them. They’ll need to know their:

Understanding these key elements – especially where an investment goal is at least five to 10 years away – could help to make a case for investing. Your clients could find their investment helps them to make inflation-beating returns in a climate where the biggest risk is not taking any risk at all.

Even with a clear idea of their risk profile, loss capacity, and a definite goal to aim for, though, the risks involved in investment can be stressful.

Usually, stress and worry can be avoided by following three basic investment rules:

Staying calm can help your clients avoid emotional, knee-jerk reactions that could lead to losses.

With the UK economy still recovering from the effects of the coronavirus pandemic, a continuing cost of living crisis and an ongoing war in Ukraine, the above lessons could be even more crucial.

Market volatility is often a result of investor uncertainty and that could well continue in the short-term.

Get in touch

If you have clients who would benefit from help with navigating the current economic climate, please get in touch. Email enquiries@boolers.co.uk or call 0116 240 7070.

Please note

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.