Richard Borrington

Reveal Menu

Why nearly half of financial advisers worry their pensioner clients are withdrawing too much

The findings of a recent report, published by FTAdviser, confirm that nearly half of advisers (47%) worry that their clients are withdrawing too much from their pensions. This marks a 19% increase since advisers were last asked the question in 2018.

Failing to effectively manage pension withdrawals can have huge consequences for your clients, from overpaying tax to running out of money in retirement.

Expert advice, if followed, can help your clients to manage their pensions.

Keep reading to find out how.

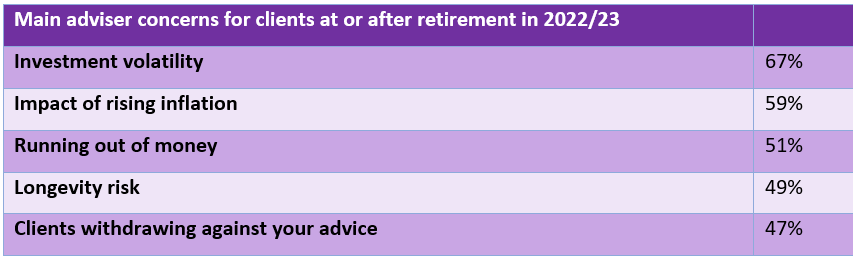

Being adaptable to the changing economic climate is key

Increased flexibility at retirement since the introduction of Pension Freedoms legislation has placed more emphasis on client budgeting.

This can be difficult in a stable financial climate but is even trickier currently. This is reflected in the top five concerns of advisers, which include the effects of rising inflation, market volatility, and increased life expectancy.

Source: FTAdviser

Let’s take a closer look at a couple of these concerns.

Investment volatility

Flexi-access drawdown allows your clients to withdraw the amount they need, as and when they need it.

The amount they don’t take remains invested. This gives those funds the chance to see further investment returns, but as with any investment, there is risk attached. Values can fall as well as rise.

Current market volatility – associated with the war in Ukraine, Covid recoveries, and China’s economic slowdown among other factors – makes this harder to manage.

Withdrawing when the markets are low means selling more units to achieve the same level of income. This can deplete your clients’ funds more quickly than they realise.

Taking too much out in the current climate could also prove problematic, as funds feel the pinch of inflation.

Rising inflation

Latest forecasts from the Bank of England (BoE) suggest that inflation could peak at 13% this year.

This means that the spending power of your clients’ pension pots will be greatly diminished. It also has an impact on the amounts that are withdrawn.

If your clients take out more than they need, the excess will likely sit in their savings accounts. And even after the BoE’s recent base rate increase, money held in cash is still highly likely to be losing value in real terms.

Longevity risk

At Boolers, we have decades of experience in dealing with the markets. We use cashflow modelling to help us build long-term plans aligned to client goals and risk levels.

These will account for rising life expectancies that could see your clients having to budget in retirement for 30 years or more.

Completing these calculations won’t always be easy for clients, especially when you consider that their pension outgoings are highly unlikely to be regular.

Expenditure will change throughout the decades of retirement. More worryingly, outgoings could grow significantly in later life – as care is required, for example – at the exact time that a poorly managed pension fund is beginning to dwindle.

Considering and balancing multiple factors is crucial to avoid running out of money

The above factors, along with discounting professional advice, could leave your clients at the very real risk of running out of money in retirement.

Taking a holistic approach is key.

Your clients will have multiple income streams in retirement, including the State Pension and non-pension income like investments or rent from buy-to-let properties.

A successful retirement plan will consider each of these and how they work alongside each other. The State Pension, for example, is unlikely to be your clients’ biggest source of retirement income, though it will be inflation-proofed, thanks to the triple lock.

Combining the State Pension with an escalating annuity from elsewhere could allow your clients to cover known, regular expenses like mortgage payments and household bills.

This could free up other pensions to cover discretionary expenditure. The flexibility of Pension Freedoms makes this simple to do, although as we’ve seen above, care will still need to be taken.

We can help your clients factor in changing expenditure and the potential cost of later-life care, ensuring that the mixture of options they choose is right for them.

Get in touch

If you have clients who are struggling to decide on the right pension option for them, or who are struggling to manage an option they have already chosen, please get in touch. Email enquiries@boolers.co.uk or call 0116 240 7070.

Please note

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The value of your investments (and any income from them) can go down as well as up, which would have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances. Levels, bases of and reliefs from taxation may change in subsequent Finance Acts.