Richard Borrington

Reveal Menu

Why the UK has the highest inflation rate of the G7 and what this means for your finances

In recent months, you’ll have seen that inflation has reached a 40-year high. According to the latest Office for National Statistics data, inflation in the UK has risen to 9%, with predictions suggesting it could hit double figures later in 2022.

Inflation is not just a UK problem. The Bureau of Labor Statistics report that US inflation was at 8.3% in April while the FT reports that eurozone inflation soared to a record 8.1% in the year to May.

While rising prices are affecting many nations, why is the inflation rate higher in the UK than elsewhere?

Read on to find out, and how you can inflation-proof your finances.

A perfect storm of issues has pushed UK inflation to its highest level since the 1980s

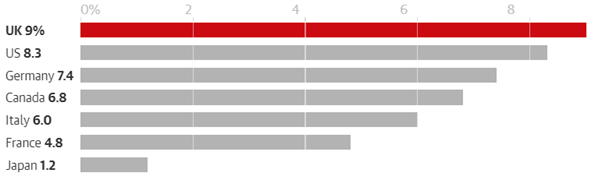

As of mid-May 2022, the UK had the highest inflation rate of any G7 country, as the chart below shows.

Source: the Guardian

So why are prices rising faster in the UK than elsewhere? There are three key reasons.

High energy prices

Back in April, the energy price cap for a typical household rose from £1,277 to £1,971 a year. And, in more worrying news, Ofgem boss Jonathan Brearley has said the cap is expected to increase to £2,800 a year from October.

As Britain is a net importer of energy, the country is more exposed to price rises. This has been exacerbated by the war in Ukraine and a post-lockdown surge in demand for oil and gas.

While these issues affect many nations, other countries have done more in response to soaring energy prices. For example, France has a 4% cap on electricity price rises and sources most of its energy needs from nuclear.

Italy has a windfall tax on energy firms and is spending around £6.8 billion to shield consumers from higher bills. Spain and Portugal are capping gas prices while Germany has cut fuel tax by 30 cents a litre, compared with Britain’s 5p cut.

While the UK government has announced £22 billion of support for high energy costs in the 2022/23 tax year, the measures do not influence the headline inflation rate.

A weak pound post-Brexit

In recent months, the pound has dropped to its lowest level against the US dollar since the early days of the pandemic. This adds to inflation by driving up the cost of imports.

In addition, disruption from the pandemic and China’s “zero Covid” policy have pushed up freight prices and caused costly delays. Companies in Britain also face additional costs from Brexit, with reams of paperwork and border delays adding to the pressure.

The Guardian reports that the thinktank UK in a Changing Europe estimates post-Brexit trade barriers pushed up food prices by 6% between December 2019 and September 2021.

Worker shortages

During the pandemic, many older people left the UK workforce. In addition, fewer foreign workers are seeking jobs in the UK after Brexit.

These labour shortages mean that companies are being forced to increase pay to attract and retain talent. This adds to their wage bills, leading them to raise the prices they charge for goods and services.

The Guardian reports that annual average pay growth, excluding bonuses, has risen to 4.2%. This is among the fastest rates for a decade.

How investing can help you to inflation-proof your wealth

In simple terms, high inflation reduces the spending power of your money.

At the current rate of 9%, goods and services that cost you £1,000 a year ago would cost you £1,090 today. If your earnings or investment returns are not keeping pace, you are worse off in real terms.

While the Bank of England have raised interest rates four times since December, Moneyfacts reports that, as of 2 June 2022, the best easy access savings account paid just 1.3%.

So, if you had invested £1,000 a year ago, you would have just £1,013 today. So, you can see that your savings are losing value in real terms.

One way that you can try and inflation-proof your wealth is to invest it.

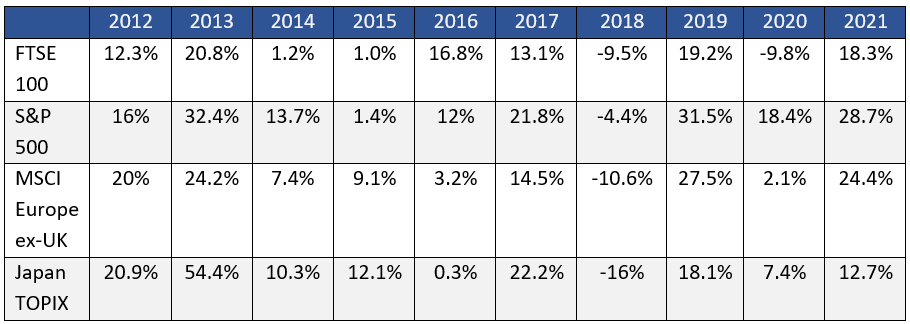

The table below shows the annual return of some of the major stock indices in the 10 years leading up to 2021 and shows that, with one or two exceptions, stock markets tended to produce positive annual returns during the period.

Source: JP Morgan, FTSE, MSCI, Refinitiv Datastream, Standard & Poor’s, TOPIX, J.P. Morgan Asset Management. All indices are total return in local currency, except for MSCI Asia ex-Japan and MSCI EM, which are in US dollars. Past performance is not a reliable indicator of current and future results. Data as of 31 January 2022.

We can help you decide which investing strategy will work for you, based on your goals, time frame, and attitude to risk.

Factor inflation into your pension withdrawals

If you’ve already retired, high inflation might mean you need to draw a higher income from your pension than you expected, just to maintain the same standard of living.

However, doing this could mean your retirement fund is at risk of running out earlier than anticipated.

To demonstrate this, consider the chart below, which shows the effects of inflation at different rates on a £100,000 pension pot if you took £5,000 a year on top of your State Pension.

Source: the Telegraph

As you can see, if inflation remained at 0% and your invested cash grew by 4% a year net of charges, you would deplete your fund after 37 years.

However, if inflation was at 7% – even lower than it is now – you would need to increase your income by 7% every year to maintain your lifestyle. This would deplete your pot in just 16 years.

Managing inflation and ensuring the withdrawals you take from your fund are sustainable will help you avoid running out of money in later life.

We use cashflow modelling software and can show you, in black and white, how periods of high inflation or stock market volatility will affect your future financial position.

Get in touch

Boolers can help you devise a financial plan that tackles inflation head on. If you would like to discuss your investment options, or how to ensure your pension withdrawals are sustainable, please contact us today.