Richard Borrington

Reveal Menu

5 financial lessons we learned in 2021

2021 has been an eventful year. From moments of sporting greatness to petrol shortages, political upheaval and the continued threat of the coronavirus pandemic, there has been plenty to keep tabs on.

As the economy continued its faltering recovery, the year also saw two budgets and various government announcements on pensions and taxation.

Here are five financial lessons you and your clients can take from 2021.

1. Tax freezes will hit many of us as the economic recovery from Covid continues

Tax freezes arrived early in the year as the chancellor delivered his Spring Budget back in March. Juggling the need for continued Covid support and to restart the country’s economy, Rishi Sunak opted for several stealth tax rises.

By freezing the Lifetime Allowance, the Capital Gains Tax Allowance, and the Inheritance Tax nil-rate and residence nil-rate band until at least 2026, the chancellor was taking the long view.

Over the next six years, the LTA freeze alone is expected to raise close to £1 billion for the Treasury, while five years of house price rises will see the numbers experiencing an IHT liability on death rise dramatically.

The Health and Social Care Levy was also announced, increasing National Insurance (NI) for employers, employees, and those workers over State Pension Age (the latter being asked to make NI contributions for the first time).

The need to manage pensions, investments, and estate planning in a tax-efficient way will become increasingly important, even as it becomes trickier.

Boolers can help your clients to spread their risk, wealth, and tax liabilities efficiently.

2. Rising inflation threatens cash savings and could suggest it’s time to invest

The Bank of England’s (BoE’s) 2% inflation target came under threat early in 2021. In April, inflation doubled, rising from 0.7% to 1.5%. By May, the BoE’s target was breached, when it reached 2.1%.

The cost of living has risen at its quickest rate in a decade, as energy bills soar and the cost of eating out, as well as prices for raw materials in factories increase. Inflation sat at 4.2% in October and yet some commentators expect it to peak above 5%, possibly around April 2022.

With the BoE’s base rate still at a historic low of 0.1%, rising inflation is unwelcome news for your clients’ cash savings. Money held in cash is effectively losing value in real terms, its interest growth lagging way behind the accelerating cost of living.

2021 has made clear the risk inherent in taking an insufficient amount of risk. Investment offers a greater chance of matching or even beating inflation, but your clients will need to understand their risk profile, their capacity for loss, and the best way to invest based on their long-term goals.

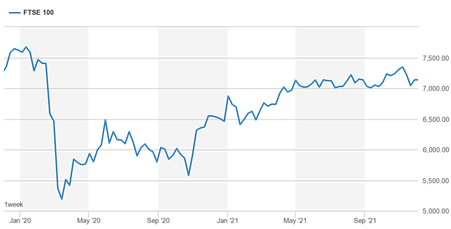

3. Patience is crucial, as is remembering that investment is a long-term proposition

The economic impact of the coronavirus in 2020 has been well-documented. From a pre-pandemic price of 7,674.56, the index suffered its biggest single-day drop in 30 years in March 2020.

Since limping above 7,000 in May 2021, the index has managed to remain above this threshold, though not without fluctuations.

Source: London Stock Exchange

The important thing for your clients to remember is that investing is a long-term proposition. It should only ever be entered into with a clear goal in mind, and one that is at least five years away.

Short-term blips in the market are to be expected, whatever the nature of the force that drives them. Having the patience and confidence to remain invested during these periods gives your clients the best chance of benefiting from future upturns in the market.

Those investors who sold big in 2020 would have missed out on the improved market position of 2021, even though average performance remains below that of the five years before the pandemic.

4. The unexpected can happen at any time, so financial protection is key

Back in October 2020, we looked at the protection products your clients need to withstand a financial shock and those lessons remain valid today.

While the vaccine – and now the booster vaccination – rollout has been a tremendous success during 2021, the emergence of new strains continues to put pressure on the NHS and highlight that the virus is still very much with us.

Your clients might consider income protection, critical illness cover or life cover.

At Boolers, we can help your clients understand the protection they – and their families – have and plug any gaps, ensuring they maintain financial stability whatever 2022 brings.

5. Financial scams continue to rise with devastating financial and emotional consequences

Despite a huge rise in scams in 2020, fraud figures have continued to increase this year.

As scammers get smarter, avoiding falling victim becomes trickier. FTAdviser recently confirmed that pension scam victims lost almost £51,000 on average in the first half of 2021. Meanwhile, UK Finance reported that authorised push payment scams cost victims more than £355 million, with impersonation scams up 129%.

Clients should be aware of the FCA’s ScamSmart site and the FCA register but it is also crucial that they seek expert financial advice, especially if they receive offers of pension or investment opportunities that seem too good to be true.

Investment and pension losses can have huge financial implications, as well as detrimentally affecting emotional wellbeing and mental health.

Get in touch

If you have clients who would benefit from help managing pensions and investments, putting financial protection in place, or gaining the confidence to recognise scam red flags, please get in touch. Email enquiries@boolers.co.uk or call 0116 240 7070.

Please note

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.