Chris Ball

Reveal Menu

5 ways financial advice can help you manage your tax bill as a high earner

According to Professional Adviser, Treasury Inheritance Tax (IHT) receipts topped £701 million in May 2024. Meanwhile, the Guardian confirms that basic-rate taxpayers have increased by more than 2 million since 2021/22, with around 1.9 million UK workers and pensioners pushed into the higher-rate bracket.

With thresholds frozen, tax receipts rising, and a cost of living crisis ongoing, ensuring that your financial plan is tax-efficient is more important than ever, especially as a high earner.

Here are five tax tips to consider.

1. Be sure to claim the tax relief you are due on your pension contributions

Your pension is incredibly tax-efficient, but you’ll want to be sure you’re making the most of its efficiencies.

The Annual Allowance, which stands at £60,000 for the 2024/25 tax year (or 100% of your earnings, if lower), is the total amount you can contribute to your pension in a single tax year without an additional tax charge. The allowance includes personal and employer contributions, as well as tax relief.

Tax relief is applied automatically to pension contributions at the basic rate of 20%. But if you’re a higher- or additional-rate taxpayer, you can claim extra relief. This is especially important if you’ve recently changed tax bracket.

At the basic rate, a £100 increase to your pension pot costs you just £80, with the additional £20 provided by the government. If you pay Income Tax at a higher rate, you can use your self-assessment tax return to claim more relief.

A £100 increase to your pension pot will cost you £60 as a higher-rate taxpayer (paying Income Tax at 40%) and just £55 if you pay the additional rate of 45%.

In February 2023, PensionsAge confirmed that unclaimed tax relief reached £1.3 billion over the five years to 2020/21. In 2020/21, higher-rate taxpayers failed to claim £425 each on average, while additional-rate taxpayers were down £527 each.

2. Increasing pension contributions could help you to recover some of your Personal Allowance

The Personal Allowance is the amount you can earn before Income Tax becomes payable.

It has been set at £12,570 since 2022. Rishi Sunak used his 2021 Spring Budget to announce a freeze on the Personal Allowance until at least 2025/26.

Your Personal Allowance goes down, though, by £1 for every £2 that your adjusted net income is above £100,000. If your income exceeds £125,140, your allowance drops to zero.

You might consider paying more into your pension. This takes advantage of your pension’s tax efficiency, as already discussed, while also decreasing your net income. A significant drop in net income might be enough to recover some of your Personal Allowance and lower your Income Tax bill.

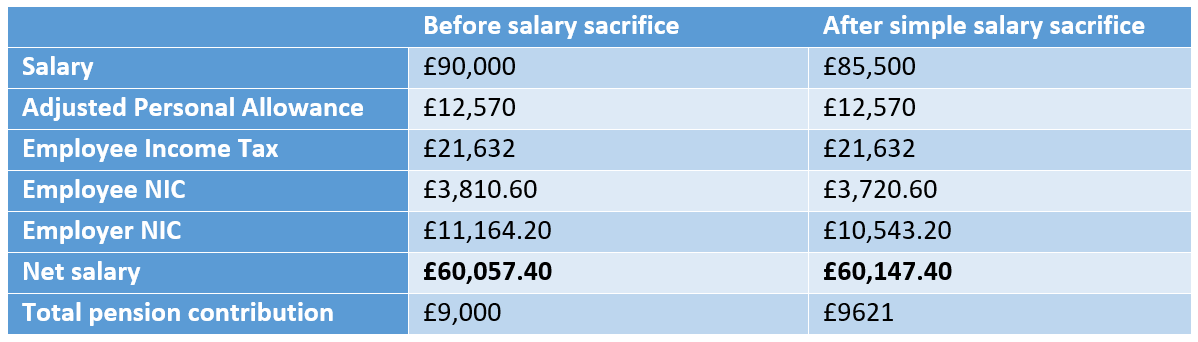

3. Consider salary sacrifice to decrease your National Insurance contributions and increase your take-home pay

Salary sacrifice allows you to give up a portion of your pay in exchange for a cash benefit, like pension contributions.

A reduced salary will likely mean lower National Insurance contributions (NICs) and could lower your Income Tax bill. You might even see your take-home pay rise.

Here is a worked example using Legal & General’s (L&G) retirement calculator, showing the effect of salary sacrifice on pre-tax earnings of £90,000. Employer and employee contributions are both set at 5%.

Source: L&G

As you can see, the effect of reduced NICs is greater take-home pay, while also increasing your pension savings, helping to secure your dream financial future once your career ends.

4. Be sure you understand the recent changes to High-Income Child Benefit Charge rules

The previous government used its 2024 Spring Budget to make changes to child benefit, increasing the amount you can earn before the benefit starts to reduce.

Previously, child benefit ceased when one parent earned more than £60,000. This has now increased to £80,000. While the benefit used to begin to be cut when one parent earned £50,000, this has been increased to £60,000.

As a higher earner, you might consider whether increased pension contributions could reduce your income below these new thresholds, helping to mitigate the impact of the High Income Child Benefit Charge (HICBC). This could be especially important for a single parent.

Under current rules, a household in which two parents earn £60,000 (£120,000 total income) wouldn’t trigger the HICBC, while a single parent with a household income of just over £60,000 will see their benefit amount reduced.

5. The importance of tax-efficient estate planning

As we have already seen, freezes to the nil-rate and residence nil-rate bands have already led to a huge increase in the Treasury’s IHT receipts.

Last July, Simon wrote about three useful ways to cut Inheritance Tax and leave more money to your loved ones, and this is becoming more important than ever.

With allowances frozen and the so-called “great wealth transfer” underway, tax-efficiently managing your estate should help to ensure that your hard-earned money goes where you want it to go. You’ll also have peace of mind that your loved ones won’t be left with a large IHT tax bill when you’re gone.

Get in touch

Boolers’ expert financial advice can help with whatever tax questions you have so be sure to speak to us if you think your tax bill could be reduced.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances. Workplace pensions are regulated by The Pension Regulator.